Scottish and Southern Energy plc, the UK's second largest power company, has completed the acquisition of Slough Heat and Power Ltd from SEGRO plc for a total cash consideration of £49.25m. The 101MW CHP plant is the UK’s largest dedicated biomass energy facility fueled by wood chips, biomass and waste paper. Part of the plant is contracted under the Non Fossil Fuel Obligation and part of it produces over 200GWH of output qualifying for Renewable Obligation Certificates (ROCs), which is equivalent to around 90MW of wind generation.

Scottish and Southern Energy plc, the UK's second largest power company, has completed the acquisition of Slough Heat and Power Ltd from SEGRO plc for a total cash consideration of £49.25m. The 101MW CHP plant is the UK’s largest dedicated biomass energy facility fueled by wood chips, biomass and waste paper. Part of the plant is contracted under the Non Fossil Fuel Obligation and part of it produces over 200GWH of output qualifying for Renewable Obligation Certificates (ROCs), which is equivalent to around 90MW of wind generation.

Africa: 2008 promises good returns for farmers

Last year, the WorldWatch Institute made the counterintuitive and controversial suggestion that high prices for agricultural commodities, partly boosted by biofuels, will benefit the world's poorest because the vast majority of them are farmers. Writing for the Nairobi based Business Daily, Dominique Patton hints at the same possibility, but stresses the benefits of high farm commodity prices will mainly trickle down to 'investor interests'.

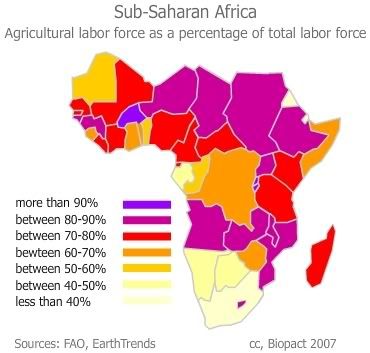

Last year, the WorldWatch Institute made the counterintuitive and controversial suggestion that high prices for agricultural commodities, partly boosted by biofuels, will benefit the world's poorest because the vast majority of them are farmers. Writing for the Nairobi based Business Daily, Dominique Patton hints at the same possibility, but stresses the benefits of high farm commodity prices will mainly trickle down to 'investor interests'.It remains to be seen whether African smallholders in difficult and underdeveloped markets will see any of these positive effects reaching them anywhere soon. The bulk of Africa's population makes a living off the land (map, click to enlarge), but only a fraction of these farmers are directly connected to world markets. However, those who are, are benefiting from unprecedented strong prices and finally see the light at the end of a dark tunnel that has kept many of them in poverty for so long. For decades, agricultural prices have trended downwards, hitting developing country farmers particularly hard.

In any case, writes Patton, African producers of almost all agricultural commodities can expect strong prices on global markets next year, with growing investor interest boosting demand-related increases.

Wheat, corn and soy have all rallied in recent weeks and analysts say grains will continue to be hot into the New Year. When Barclays Capital asked 150 clients at a commodities conference this month which sectors they expected to produce the highest returns next year, 45 per cent voted for agricultural markets, well above the 19 per cent going for precious metals.

Investor interest, a new phenomenon, is largely thanks to strong fundamentals. Robust demand in emerging economies has drawn down stocks to record lows and despite a record food harvest this year, farmers cannot replenish grain stores fast enough to buffer them from weather-related shocks. In China, cereal stocks fell significantly between 2000 and 2004 and have not recovered in recent years.

Its booming economy means people are spending more on meat, and feeding more animals requires greater amounts of corn and soy. This year China became a net importer of corn, also known as maize.

That is one of the reasons why corn prices will stay high into 2008, despite a substantial rise in plantings in the US, says Luke Chandler, a commodities analyst at Rabobank in Australia. The other is the pressure from biofuels. "The US already uses a quarter of its crop for biofuel and there is talk of it increasing this to 40 or 50 per cent by 2020."

Corn prices passed record prices of $175 a tonne earlier this year, and although it has fallen from its peak, at $150 a tonne it is still 50 per cent above the average for 2006.

Weather forecasts suggest that next year's production may be hurt by dry weather, says James Nuttall, director of the UBS bank's commodities business in London. "We could see a fairly dry period in some of the corn-growing regions in North America and that could lead to production volatility."

All that creates a tempting world market for African farmers who manage to produce a surplus for export. Corn production could decline again this year if farmers switch to growing wheat, now priced at $400 per ton after bad weather conditions in Europe and Australia drastically reduced supplies:

energy :: sustainability :: biomass :: bioenergy :: biofuels :: ethanol :: biodiesel :: agricultural commodities :: Africa ::

energy :: sustainability :: biomass :: bioenergy :: biofuels :: ethanol :: biodiesel :: agricultural commodities :: Africa :: Rabobank's Mr Chandler says there could be an extra 40-50 million tons of wheat entering the market next year and that would take much of the squeeze out of the market. Farmers should expect high volatility in pricing however. There may be brakes put on using corn for biofuels in countries like China where food security is a major issue.

Biofuel production is leading a major structural change to the soft commodities market. While cereal use for food and feed increased by four and seven per cent respectively since 2000, the use of cereals for industrial purposes, such as making biofuels, increased by more than 25 per cent, according to a recent report from the International Food Policy Research Institute (IFPRI). That shows the extent to which demand has changed in recent years, and why supply responses must be much quicker.

Biofuels are also driving strong investor interest in oilseeds. Palm oil and soybean oil, both sources of alternative energy, are increasingly attractive to clients, says Mr Nutall at UBS.

This year's price movements show why. Average US soybean and soy oil prices have increased 41 per cent this year, while Malaysian palm oil prices are up by 54 per cent and EU rapeseed prices are 20 per cent higher.

Soybeans have seen a recent rally based on record crude oil levels serving as a reminder of the need for fuel substitutes. Palm oil is attractive owing to its relatively long growing time, which makes it slower to respond to supply shortages.

Cotton has also benefited from biofuel demand, indirectly. Long a loss-making crop in Kenya, prices for the 2007 cotton are expected to jump by up to a quarter as acreage in the US declines with growing production of the higher priced cereals.

"Cotton acreage is down 18 per cent and some people expect it to fall even further. That has helped reduce some of the supply and demand imbalance and eroded a build-up of inventories," says Mr Chandler.

A steep increase in prices on the New York Board of Trade suggests traders are counting on more positive fundamentals for cotton too.

Consumption is on an upward trend in emerging economies like China and India although there is some evidence that higher prices are dampening demand among processors who can switch to alternatives.

"It is very much one of the markets in balance right now," says Mr Chandler. How it works out could be important for the regeneration of Kenya's cotton sector.

Like other crops, cotton is being added to a basket of commodities as investors try to hedge against rising inflation.

"We're seeing lots of clients looking for long-term exposure," says Mr Nuttall of UBS. "There's very strong appetite for agricultural and soft commodities. They are a natural hedge against food inflation."

There are signs that soft commodities, seeing much less growth beside the agriculturals, are going to pick up too. Coffee has already gained a high profile as prices on international markets surged to near 10-year highs in volatile trade this year.

That was mostly fuelled by speculation of a downturn in arabica's biennial production cycle in the world's biggest producer Brazil. It now appears to have produced above expectations.

Robusta is more bullish for 2008, says Mr Nuttall, driven by lower output from Vietnam and rising demand in Asia. But higher Arabica quality in Kenya should still leave farmers happy with prices.

Opinions on sugar remain divided. The market is one of the main underperformers among the agricultural range thanks to a huge surplus in India and Brazil. The average price for 2007 was down 33 per cent on the prior year.

But there has been some rallying in prices in recent weeks and some traders are bullish on both raw and white sugar based on higher consumption in Asian diets and in ethanol production in Brazil, and a drop in Indian production.

Unlike other commodities such as precious metals, softs and agriculturals have much more capacity to react to supply shortages. It can take years to find a new mine and then extract the metal but most crops - apart from coffee and cocoa - can be planted and grown in a year. More elastic supply means prices are unlikely to reach those seen recently in metals.

"Prices will keep a premium versus the historical trend but agriculture is cyclical," predicts Mr Chandler. "Supply can respond and prices act as a strong signal to farmers."

But rising investor interest is pushing soft commodity prices away from straightforward supply-demand equations. Last year the volume of traded global agricultural futures and options rose by almost 30 per cent, according to IFPRI. The volume is set to keep growing as bullish supply and demand conditions continue into 2008.

References:

Business Daily: Africa: 2008 Promises Good Returns for Farmers - January 1, 2008.

Biopact: Worldwatch Institute: biofuels may bring major benefits to world's rural poor - August 06, 2007

Article continues

posted by Biopact team at 1:40 PM

0 comments

links to this post

![]()

![]()

Wednesday, January 02, 2008

First biomass plant in Bangladesh generates rural electricity from rice husks

The green power plant, the first ever its kind in Bangladesh, is a 250 kW biomass gasification facility that generates renewable electricity from abundant agricultural residues such as rice husks. IDCOL provided concessionary loans and grants, sourced from IDA and the Global Environmental Facility (GEF), for a total project costy of 25 million taka (€250,000) of which the World Bank provided 60%.

DreamsPower is the initiative of Asaduzzaman Manik, a poultry farmer who experienced great difficulties in keeping his business running without electricity. Fed up with the status quo, he decided to create his own 'micro energy company'.

Being located in an un electrified area, the plant is now supplying environmentally friendly grid quality power to about 500 households and commercial entities for the first time. The unique plant in the town supplies all the required energy in a decentralised manner, without the need for backup from other sources. A total of 220 consumers have been connected to the local grid, while another 2,300 applicants await connections.

Through the Rural Electrification and Renewable Energy Development Project, commonly known as RERED, the World Bank is supporting these types of initiatives in Bangladesh. Under this project, IDCOL is installing thousands of solar home energy and biogas systems. The Rural Electrification Board now wants to replicate the effort for biomass power plants.

According to Asaduzzaman Manik, managing director of DreamsPower, at present only about 38% of the population in Bangladesh has access to electricity. Expanding rural electrification is key to the prosperity and development of rural areas:

While growth in electricity consumption is directly related to economic growth, electrification is also required to attain Millennium Development Goals: power is needed to maintain the 'cold chain' for vaccines; the likelihood of babies surviving to five years is significantly higher in villages with electricity than those without; electricity also opens new avenues for job creation and thus increases income.

The World Bank hopes that IDCOL will promote biomass power plants in rural Bangladesh the same way it promoted solar home systems. The lessons learnt from installing this plant could be effectively used while preparing other biomass plants. This will certainly reduce the challenges for the next entrants and can attract new entrepreneurs to install biomass power plants in rural Bangladesh to meet the electricity demand. This will also create employment opportunities in rural Bangladesh.

Besides supporting the conventional grid based electricity sector, Bangladesh’s comparative advantage in the renewable energy resources is appreciated and the WorldBank says it is willing to support Bangladesh’s future needs to develop its renewable energy sector if the government so requests.

Given the lack of adequate power generation capacity in Bangladesh, promoting this type of decentralized renewable energy power plants will add to the country’s energy security and shall meet energy demand.

Picture: rice is Bangladesh's first crop, yielding an abundant stream of residues, such as the rice husks transported in this barge, that can be efficiently used in modern bioenergy systems.

References:

WorldBank: First Ever Biomass Power Plant in Bangladesh - January 2, 2007.

Daily Star: First-ever rice-husk biomass power plant begins commercial operation - January 2, 2008.

Article continues

posted by Biopact team at 2:49 PM 0 comments links to this post