Petro-Canada and GreenField Ethanol have inked a long-term deal that makes Petro-Canada the exclusive purchaser of all ethanol produced at GreenField Ethanol's new facility in Varennes, Quebec. The ethanol will be blended with gasoline destined for Petro-Canada retail sites in the Greater Montreal Area.

Petro-Canada - June 27, 2007.

According to a study by the Korean Energy Economics Institute, biodiesel produced in Korea will become cheaper than light crude oil from 2011 onwards (678 won/liter versus 717.2 won/liter). The study "Prospects on the Economic Feasibility of Biodiesel and Improving the Support System", advises to keep biodiesel tax-free until 2010, after which it can compete with oil.

Dong-A Ilbo - June 27, 2007.

Kreido Biofuels announced today that it has entered into a marketing and distribution agreement with Eco-Energy, an energy and chemical marketing and trading company. Eco-Energy will purchase Kreido Biofuels’ biodiesel output from Wilmington, North Carolina, and Argo, Illinois, for a minimum of 3 years at current commercial market prices, as well as provide Kreido transportation and logistics services.

Business Wire - June 27, 2007.

Beijing Tiandi Riyue Biomass Technology Corp. Ltd. has started construction on its new fuel ethanol project in the county of Naiman in Inner Mongolia Autonomous Region's Chifeng City, the company's president told Interfax today.

Interfax China - June 26, 2007.

W2 Energy Inc. announces it will begin development of biobutanol from biomass. The biofuel will be manufactured from syngas derived from non-food biomass and waste products using the company's plasma reactor system.

Market Wire - June 26, 2007.

Finland based Metso Corporation, a global engineering firm has received an order worth €60 million to supply two biomass-fired power boilers to Portugal's EDP Producao - Bioeléctrica, S.A. The first boiler (83 MWth) will be installed at Celbi’s Figueira da Foz pulp mill and the second boiler (35 MWth) at Caima’s pulp mill near the city of Constância. Both power plants will mainly use biomass, like eucalyptus bark and forest residues, as fuel to produce together approximately 40 MWe electricity to the national grid. Both boilers utilize bubbling fluidized bed technology.

Metso Corporation - June 26, 2007.

Canada's New Government is investing more than $416,000 in three southern Alberta projects to help the emerging biofuels industry. The communities of Lethbridge, Drumheller and Coalhurst will benefit from the projects. Through the Biofuels Opportunities for Producers Initiative (BOPI), the three firms will receive funding to prepare feasibility studies and business plans to study the suitability of biofuels production according to location and needs in the industry.

MarketWire - June 26, 2007.

U.S. Energy Secretary Samuel Bodman is expected to announce today that Michigan State and other universities have been selected to share $375 million in federal funding to develop new bioenergy centers for research on cellulosic ethanol and biomass plants. More info soon.

Detroit Free Press - June 26, 2007.

A Kerala based NGO has won an Ashden Award for installing biogas plants in the state to convert organic waste into a clean and renewable source of energy at the household level. Former US vice president Al Gore gave away the award - cash prize of 30,000 pounds - to Biotech chief A. Saji at a ceremony in London on Friday.

New Kerala - June 25, 2007.

AltraBiofuels, a California-based producer of renewable biofuels, announced that it has secured an additional US$165.5 million of debt financing for the construction and completion of two plants located in Coshocton, Ohio and Cloverdale, Indiana. The Coshocton plant's capacity is anticipated to reach 60million gallons/year while the Cloverdale plant is expected to reach 100 million gallons/year.

Business Wire - June 23, 2007.

Brazil and the Dominican Republic have inked a biofuel cooperation agreement aimed at alleviating poverty and creating economic opportunity. The agreement initially focuses on the production of biodiesel in the Dominican Republic.

Dominican Today - June 21, 2007.

Malaysian company Ecofuture Bhd makes renewable products from palm oil residues such as empty fruit bunches and fibers (more here). It expects the revenue contribution of these products to grow by 10% this year, due to growing overseas demand, says executive chairman Jang Lim Kuang. 95% of the group's export earnings come from these products which include natural oil palm fibre strands and biodegradable mulching and soil erosion geotextile mats.

Bernama - June 20, 2007.

Argent Energy, a British producer of waste-oil based biodiesel, announced its intention to seek a listing on London's AIM via a placing of new and existing ordinary shares with institutional investors. Argent plans to use the proceeds to construct the first phase of its proposed 150,000 tonnes (170 million litres) plant at Ellesmere Port, near Chester, and to develop further plans for a 75,000 tonnes (85 million litres) plant in New Zealand.

Argent Energy - June 20, 2007.

The first conference of the European Biomass Co-firing Network will be held in Budapest, Hungary, from 2 to 4 July 2007. The purpose of the conference is to bring together scientists, engineers and members of public institutions to present the current state-of-the-art on biomass co-firing. Participants will also discuss future trends and directions in order to promote awareness of this technology as a sustainable energy supply, which could decrease the dependency on fossil fuels and guarantee a decentralised source of energy in Europe. The conference is supported by the EU-funded NETBIOCOF (Integrated European Network for Biomass Co-firing) project.

NetBioCof - June 19, 2007.

Green Energy Resources predicts US$50 per ton biomass woodchip prices within the next twelve months. The current US price level is between $25-32 per ton. Demand caused by the 25-30 new power plants planned in New England by 2010 does not include industry, institutions, universities, hospitals or conversions from natural gas, or cellulostic ethanol. Procurement of woodchips will be based on the delivery capacity of suppliers not local prices for the first time in history. Green Energy has been positioning in New England with rail and port locations to meet the anticipated sector expansion.

MarketWire - June 19, 2007.

In the first major initiative in the US to build a grassroots communications network for the advancement of biofuels adoption, a new national association called The American Biofuels Council (ABC) has been formed.

American Biofuels Council - June 19, 2007.

The Novi Sad-based Jerković Group, in partnership with the Austrian Christof Group, are to invest about €48 million (US$64.3m) in a biodiesel plant in Serbia.

Property Xpress - June 19, 2007.

Biodiesel producer D1 Oils, known for its vast jatropha plantations in Africa and Asia, is to invest CNY 500 to 700 million (€48.9-68.4 / US$65.5-91.7) to build a refinery in Guangxi Zhuang autonomous region, in what is expected to be the first biodiesel plant in the country using jatropha oil as a feedstock.

South China Morning Post - June 18, 2007.

After Brazil announced a record sugar crop for this year, with a decline in both ethanol and sugar prices as a result, India too is now preparing for a bumper harvest, a senior economist with the International Sugar Organization said. Raw sugar prices could fall further towards 8 cents per lb in coming months, after their 30% drop so far this year. Converting the global surplus, estimated to be 4 million tonnes, into ethanol may offer a way out of the downward trend.

Economic Times India - June 18, 2007.

After Brazil announced a record sugar crop for this year, with a decline in both ethanol and sugar prices as a result, India too is now preparing for a bumper harvest, a senior economist with the International Sugar Organization said. Raw sugar prices could fall further towards 8 cents per lb in coming months, after their 30% drop so far this year. Converting the global surplus, estimated to be 4 million tonnes, into ethanol may offer a way out of the downward trend.

Economic Times India - June 18, 2007.

A report from the US Department of Agriculture Foreign Agricultural Services (USDA FAS) estimates that the production of ethanol in China will reach 1.45 million tonnes (484 million gallons US) in 2007, up 12% from 1.3 million tonnes in 2006. Plans are to increase ethanol feedstocks from non-arable lands making the use of tuber crops such as cassava and sweet sorghum.

USDA-FAS - June 17, 2007.

The Iowa State University's Extension Bioeconomy Task Force carried out a round of discussions on the bioeconomy with citizens of the state. Results indicate most people see a bright future for the new economy, others are cautious and take on a distanced, more objective view. The potential for jobs and economic development were the most important opportunities identified by the panels. Iowa is the leading producer of corn based ethanol in the US.

Iowa State University - June 16, 2007.

Biofuel producer D1 Oils Plc, known for establishing large jatropha plantations on (degraded land) in Africa and Asia, said it was in advanced talks with an unnamed party regarding a strategic collaboration, sending its shares up 7 percent, after press reports linking it with BP. Firms like BP and other large petroleum companies are keen to secure a supply of biofuel to meet UK government regulations that 5 percent of automotive fuel must be made up of biofuels by 2010.

Reuters UK - June 15, 2007.

Jean Ziegler, a U.N. special rapporteur on the right to food, told a news briefing held on the sidelines of the U.N. Human Rights Council that "there is a great danger for the right to food by the development of biofuels". His comments contradict a report published earlier by a consortium of UN agencies, which said biofuels could boost the food security of the poor.

Reuters - June 15, 2007.

The county of Chicheng in China's Hebei Province recently signed a cooperative contract with the Australian investment and advisory firm Babcock & Brown to invest RMB480 million (€47.2/US$62.9 million) in a biomass power project, state media reported today.

Interfax China - June 14, 2007.

A new two-stroke ICE engine developed by NEVIS Engine Company Ltd. may nearly double fuel efficiency and lower emissions. Moreover, the engine's versatile design means it can be configured to be fuelled not only by gasoline but also by diesel, hydrogen and biofuels.

PRWeb - June 14, 2007.

Houston-based Gulf Ethanol Corp., announced it will develop sorghum as an alternative feedstock for the production of cellulosic ethanol. Scientists have developed drought tolerant, high-yield varieties of the crop that would grow well in the drier parts of the U.S. and reduce reliance on corn.

Business Wire - June 14, 2007.

Bulgaria's Rompetrol Rafinare is to start delivering Euro 4 grade diesel fuel with a 2% biodiesel content to its domestic market starting June 25, 2007. The same company recently started to distributing Super Ethanol E85 from its own brand and Dyneff brand filling stations in France. It is building a 2500 ton/month, €13.5/US$18 million biodiesel facility at its Petromidia refinery.

BBJ - June 13, 2007.

San Diego Gas & Electric (SDG&E), a utility serving 3.4 million customers, announced it has signed a supply contract with Envirepel Energy, Inc. for renewable biomass energy that will be online by October 2007. Bioenergy is part of a 300MW fraction of SDG&E's portfolio of renewable resources.

San Diego Gas & Electric - June 13, 2007.

The World Wildlife Fund (WWF) today announced its opposition to a plan by Planktos Inc. to dump iron dust in the open ocean west of the Galapagos Islands. The experiment seeks to induce phytoplankton blooms in the hopes that the microscopic marine plants will absorb carbon dioxide. The company is speculating on lucrative ways to combat climate change. Reports indicate that Planktos, Inc. - a for profit - is planning other large-scale iron dumping in other locations in the Pacific and Atlantic Oceans. The current experiment could negatively impact the unique marine ecosystems of the Galapagos Islands.

Scientists have warned against this type of 'geo-engineering' schemes, which have - in the case of iron seeding - clearly shown not to work and could harm ocean life (previous post). Simulations also indicate that such strategies carry considerable environmental risks and could even worsen the effects of climate change (earlier post). For these reasons, the UN's Intergovernmental Panel for Climate Change has clearly stated in its latest report that none of these techniques carry a priority to mitigate climate change (report of the IPCC's Working Group III).

There are much safer and proven ways of preventing or lowering carbon dioxide levels than dumping iron into the ocean. This kind of experimentation with disregard for marine life and the lives of people who rely on the sea is unacceptable. - Dr. Lara Hansen, chief scientist, WWF International Climate Change Program

One of those far more feasible and less risky geo-engineering options is the implementation of carbon-negative bioenergy systems (also known as 'Bio-Energy with Carbon Storage' or BECS, see earlier post, and here, here).

According to a summary by the United States Government submitted to the International Maritime Organization, Planktos, Inc. - a for-profit company - will dump up to 100 tons of iron dust this month in a 36 square mile area located approximately 350 miles west of the Galapagos Islands. Planktos, Inc. plans to dump the iron in international waters using vessels neither flagged under the United States nor leaving from the United States so U.S. regulations such as the U.S. Ocean Dumping Act do not apply and details do not need to be disclosed to U.S. entities:

World Wildlife Fund's concern extends beyond the impact on individual species and extends to the changes that this dumping may cause in the interaction of species, affecting the entire ecosystem. There's a real risk that this experiment may cause a domino effect through the food chain. - Dr. Sallie Chisholm, microbiologist, MIT and board member, World Wildlife Fund

Shifts in the composition of species that make up plankton, the base of the marine food chain, would cause changes in all the species that depend on it.

The impact of gases released by both the large amount of phytoplankton blooms induced by Planktos, Inc. and resulting bacteria after the phytoplankton die.

Bacterial decay following the induced phytoplankton bloom will consume oxygen, lowering oxygen levels in the water and changing its chemistry. This change in chemistry could favor the growth of microbes that produce powerful greenhouse gases such as nitrous oxide.

The introduction of large amounts of iron to the ecosystem - unless it is in a very pure form, which is likely cost-prohibitive at the scales proposed - would probably be accompanied by other trace metals that would be toxic to some forms of marine life.

In the waters around the Galapagos, some 400 species of fish swim with turtles, penguins and marine iguanas above a vast array of urchins, sea cucumbers, crabs, anemones, sponges and corals. Many of these animals are found nowhere else on earth.

If you feel like protesting against Planktos Inc.'s questionable experiment - we do - then join us in writing to the company to express your concerns. Send your email to Russ George, CEO of Planktos Inc.:[email protected].

The two Danish biotechnology firms Novozymes A/S and Xergi A/S, heavily involved in the biofuels sector, have announced an agreement that enables them to collaborate on the co-development of microorganisms and environmental technologies for the optimal harvest of energy from manure products for use in the production of renewable biogas that yields electricity, heat, and fuels, as well as high-quality fertilizer. According to the Danish Board of Technology, biomethane from manure can supply 25% of the energy required by the Danish transport sector.

This initiative stems from the Danish government’s globalization strategy [*.pdf], to strengthen Denmark’s competitive abilities. The strategy includes support for business-to-business partnerships within five focus areas as formulated by the Ministry of the Environment: giant wind turbines, biofuels, potable water, hydrogen/fuel cells and industrial biotechnology.

Novozymes, a leading industrial enzyme developer, and Xergi, an innovative biogas producer, enter into the last-named partnership, established by the Minister of the Environment Connie Hedegaard. Several other private and public institutes are also participating, among them the Faculty of Agricultural Sciences at Århus University, where Xergi has recently supplied a large anaerobic digestion facility in Foulum.

We see the possibility of a new business area in manure management. Biotechnology has the potential to create increased value in this exciting new field, where energy production is combined with an environmentally friendly process to re-use manure for fertilizer. We are looking forward to our collaboration with Xergi, where we can put our skills and abilities together to shed light on the technological and business opportunities. - Rasmus von Gottberg, Vice President at Novozymes

The Partnership for Industrial Biotechnology has chosen to focus on the area of manure management. The partners identify a set of areas with positive development potential and large export possibilities so Denmark can become a leader in the global marketplace. Denmark already holds a global leadership position in both anaerobic digestion and enzyme & microorganism biotechnology, and together these two leading companies with the other partners will boost Danish environmental technology, benefiting renewable energy and the use of fertilizer globally: bioenergy :: biofuels :: energy :: sustainability :: biogas :: biomethane :: fertilizer :: enzymes :: anaerobic fermentation :: Denmark :: Through their joint effort, Novozymes and Xergi, which is jointly owned by the holding company Schouw & Co. and Hedeselskabet, will develop microorganisms and technologies to harvest the valuable components from manure in the form of energy and nutrients. The process will, in part, optimize the yield of energy from these slurries, and increase the quality of the by-product for use as fertilizer (basic flow-chart of biogas production, click to enlarge).

While Novozymes can develop microorganisms so they optimize the processes in a biogas facility, Xergi has close contact to the market and knows how to optimize the technology where it will be installed and used. By promoting and distributing both green energy and manure management technologies globally, these two companies will strengthen Denmark’s competitive advantage.

Large market possibilities In Denmark less than 5% of agricultural manure is converted to energy in the form of biogas. Of this 5%, only 50% of the energy is harvested. If all the energy stored in Danish manure could be extracted, the country could, according to the Danish Board of Technology, supply 25% of the energy required by the Danish transport sector.

The ambition and goal of the collaboration between Novozymes and Xergi is to increase substantially the yield of energy from manure so society can get enhanced access to a green, sustainable source of energy that can be used for electricity, heating and the transport, all delivered via the existing natural gas system. And beyond conserving the planet’s natural but dwindling energy resources, this biotechnology will help reduce the release of CO2.

References: Novozymes: Enzymes at Work [*.pdf] - a guide to the world of industrial enzymes and how they are used to make sustainable solutions for many industries.

According to BBC Brasil, a Chinese state-owned enterprise and a Brazilian group have signed [*Portuguese] an agreement to build two large ethanol factories in Brazil, the output of which will be entirely for the Chinese market. The venture comes at a time when China is considering reducing the production of ethanol from grains and to switch to non-food crops and biofuel imports (previous post). This Sino-Brazilian partnership is the latest in a series of Chinese investments in biofuel production abroad - with projects in the Philippines, Indonesia, Mozambique, Malaysia, and Nigeria. Like Japan, the People's Republic is securing a 'green reserve' of bioenergy located in the continents that are crossed by the equator.

China's state-owned BBCA Biochemicals, located in Anhui province (southeast China), and Brazil’s Grupo Farias, from Pernambuco state (northeast Brazil), have joined forces to set up the plants, at an investment of 390 million reais (€149/US$200 million), which are expected to come online between 2009 and 2010 and will be amongst the ten largest in Brazil. BBCA Biochemical is the sole biofuel producer authorized by the Chinese government to supply fuel ethanol to Anhui, Shandong, JiangSu and Hebei provinces. It has a domestic capacity of 440,000 tons/year in China, but now decides to produce abroad and import. The Grupo Farias currently operates 11 ethanol plants.

Each factory in the Chinese-Brazilian partnership should have a processing capacity of 5 million tons of sugarcane per year - which is large, even by Brazilian standards. Per plant, a production of between 400 and 500 million liters is expected. According to figures from the Union of Sugar Cane Industries (Unica), the country's biggest factories currently are Barra (7 million tons), Sao Martinho (6.7 million), Santa Elisa (5.9 million), Vale do Rosario (5.4 million) and Itamarati (5 million). Combined, the Sino-Brazilian venture may ship up to 1 billion liters of ethanol to China per year.

The factories are likely to be built in the northeastern Brazilian state of Maranhão.

We plan to build units that will be amongst the largest in Brazil. Because of agro-industrial scale advantages we have decided to build two separate plants. [Because of the particularities of sugarcane logistics] building a single large factory does not offer competitive advantages. It is almost certain that the plants will be located there [in Maranhão state], as there is a good area for planting cane and the port of Itaqui has the capacity to receive large ships - Eduardo Farias, the chairman of Grupo Farias.

The Itaqui port is located in the state capital city of São Luís.

Over the coming weeks the chairman of BBCA Biochemicals Anhui, Li Rong-Jie, will travel to Brazil with a group of Chinese executives to define the final details of the partnership with Grupo Farias: biofuels :: energy :: sustainability :: sugarcane :: ethanol :: biofuels trade :: Brazil :: China :: China's import taxes The Brazilian press has reported that Grupo Farias will have a majority-stake in the partnership and that the taxes on importing ethanol into China were still under discussion. “We are jointly informing the Chinese government so that it can understand that it needs to lower taxes on ethanol," Farias said.

According to figures from the Brazilian embassy in Beijing, the Chinese government’s tariff table shows that taxes on alcohol imports can vary between 30 and 40 percent.

"The current tax is actually a levy on alcoholic beverages. We are currently trying to convince the Chinese government of the fact that removing the tariff on ethanol as a fuel is in its own interest. It will boost imports of the green fuel", says Charles Tang, president of the Brazilian-Chinese Chamber of Commerce and Industry.

The Grupo Farias is a family run business with headquarters in Pernambuco. It has over 40 years of experience in the sugarcane ethanol industry.

Brazil is attracting considerable investments from Asian countries, amongst them India and Japan, with which it has export agreements.

Illustration: One of the Grupo Farias' ethanol plants, Vale Verde Itapací, in the state of Goias. Credit: Grupo Farias.

Chumporn Palm Oil Industry (CPI), Thailand's largest palm oil manufacturer, plans [*cache] to invest 500 million baht (€11.7/US$15.7) to make palm-oil based biodiesel from next year onwards.

The company is currently conducting a feasibility study on location and costs, which should be completed in 12 months, said CPI adviser Suriya Ayachanun. Construction could start soon after the study is done and the company has drawn up a financial plan.

The project looks as follows:

capacity: the biodiesel plant will produce 100,000 tonnes per year of 100% (B100) palm-oil based biofuel

feedstock: refined bleached deodorised (RBD) palm stearin, a byproduct of palm oil production (schematic, click to enlarge); CPI currently produces 54,000 tonnes of RBD palm stearin, the entire output of which will feed the biodiesel factory; the remainder will be supplied by new feedstock production

share of total production: CPI aims to produce 190,000 tonnes of crude palm oil (CPO) this year, or 19% of Thailand's total annual consumption of 978,800 tonnes; in addition, it expects to produce 180,500 tonnes of refined bleached deodorised (RBD) palm oil this year

market: the palm-oil based biodiesel will be sold both at home and abroad; B100 would be exported as an additive to countries that want to reduce the sulphur content in diesel because the toxic substance causes acid rain

The biodiesel market in Thailand has lots of room to expand because the country's Energy Ministry will force all oil refiners to mix 10% biofuel with diesel to produce B10 from 2011 onward. Conventional diesel consumption volume in 2011 and 2012 is expected to reach between 60 million and 65 million litres a day. In short, biodiesel demand will be between 2.19 and 2.37 billion liters per annum (roughly 37,700 and 41,000 barrels per day): bioenergy :: biofuels :: energy :: sustainability :: palm oil :: biodiesel :: stearin :: Thailand :: Currently, the Energy Ministry allows oil refiners to mix 2% biofuel with diesel without the need to inform consumers. Diesel demand in the country is now 56 million litres per day. According to Suriya Ayachanun lubricity additive markets are the future of palm-oil based biofuel producers.

Refinery war However, CPI refuses to sell crude palm oil to Thai Oleochemicals Co Ltd (TOL), the sole oleochemicals manufacturer in Thailand and a subsidiary of PTT Chemical Plc. The company says sales would lead to crude palm oil supply shortages to CPI's own palm oil refinery.

Recently, TOL expressed its need to buy a huge amount of crude palm oil from CPI and other producers to make oleochemicals.

TOL requires 300,000 tonnes of crude palm oil and palm kernel oil per year to produce 130,000 tonnes of fatty alcohol and glycerine, which are used as raw materials for consumer products such as soap, shampoo, lotion, toothpaste and cosmetics. The company also makes 200,000 tonnes per year of methyl ester, used in biodiesel production.

"We could make the deal with TOL if we didn't have our own palm oil refinery business," said Mr Suriya.

CPI currently exports about 10,000 tonnes of crude palm kernel oil a year to Malaysia but could shift some of that output to supply TOL if it offered good terms, he added.

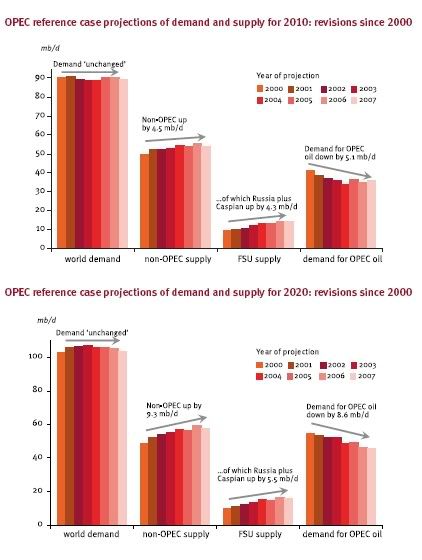

The Organisation of Petroleum Exporting Countries (OPEC) has released its World Oil Outlook 2007 [*.pdf], which contains some interesting perspectives for biofuels, tightly linked to the way OPEC will invest in future capacity expansion.

Most importantly, according to the report, the demand for OPEC crude by 2010 has been revised downwards and will be almost 1 million barrels per day (mb/d) below 2005 levels because of the rise of non-OPEC non-conventional resources (including biofuels) (click to enlarge). Thereafter, demand for OPEC oil will gradually increase. But uncertainties over demand, driven by the rise of green fuels and non-conventional resources, may have serious consequences and delay much needed investments across the entire supply chain. Especially the addition of new oil refinery capacity may get delayed.

In general, biofuels projects do not take as long to implement as refinery projects. The reference case allows for a significant medium-term increase in biofuels production. Any additional increase would further reduce required refinery throughputs and margins. Consequently, policy initiatives to support the development of biofuels may discourage refiners, as well as possibly crude oil producers, from investing in the needed capacity expansion.

The result of this scenario is high fuel product and crude oil prices, expected to remain at a level of $50-60 per barrel until 2030. This is exactly the price bracket at which biofuels made in the South (e.g. sugarcane ethanol and palm oil biodiesel) can directly, without subsidies, compete with oil.

However, if the ambitious biofuel targets in the OECD are not met, the result could be further tightness in the downstream, and possibly the upstream, and in turn, this could have a significant impact on prices, margins and volatility. Such an event would automatically kickstart biofuel production again.

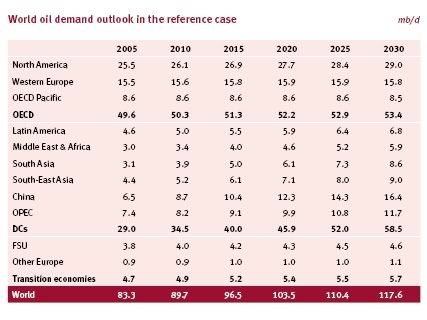

Global outlook According to the report demand for energy in general is set to continue to grow (click to enlarge) and oil is expected to maintain its leading position in meeting the world’s growing energy needs for the foreseeable future. In OPEC's reference case, with an average global economic growth rate of 3.5% per annum (purchasing power parity basis), and oil prices assumed to remain in the $50-60/b range in nominal terms for much of the projection period, oil demand is set to rise from the 2005 level of 83 mb/d to 118 mb/d by 2030.

This assumes that no particular departure in trends for energy policies and technologies takes place. This is a very important caveat for there are inherent downside risks to demand, something that is specifically addressed in the Outlook. One of these 'risks', is indeed the fast growth of biofuels and non-OPEC, non-conventional oil resources.

OECD countries, currently accounting for close to 60% of world oil demand, see a further growth of 4 mb/d by 2030, reaching 53 mb/d - mainly coming from North America. Developing countries account for most of the rise in the reference case, with consumption doubling from 29 mb/d to 58 mb/d. Asian developing countries account for an increase of 20 mb/d, which represents more than two-thirds of the growth in all developing countries.

Nevertheless, the Outlook assumes that energy poverty will remain an important issue over this period. By 2030, developing countries will consume, on average, approximately five times less oil per person, compared with OECD countries.

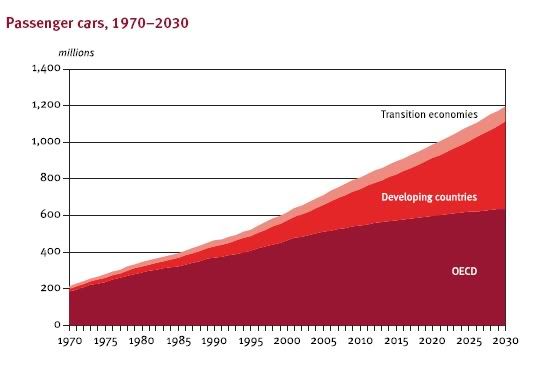

Demand per sector The transportation sector will be the main source of future oil demand increases. Growth in the OECD is expected to continue to rise, although saturation effects should increasingly have an impact upon the growth in passenger car ownership. The potential for growth in the stock of cars, buses and lorries, however, is far greater in developing countries (click to enlarge). For example, two-thirds of the world’s population currently live in countries with less than one car per 20 people. The total stock of cars is expected to rise from 700 million in 2005 to 1.2 billion by 2030, and the global volume of commercial vehicles is anticipated to more than double: biofuels :: energy :: sustainability :: ethanol :: biodiesel :: biomass :: petroleum :: oil :: OPEC :: Of the non-transportation oil use, the main expected source of increase will be in the industrial and residential sectors of developing countries, which see a combined growth to 2030 of over 11 mboe/d in the reference case. Oil use in households is closely associated with the gradual switch away from traditional fuels. This trend is expected to continue, especially in the poorer developing countries of Asia and Africa, with the urbanisation movement throughout the developing world central to the shift towards commercial energy.

Despite the expected continued growth in electricity production and consumption, oil demand in this sector will experience no significant growth.

No 'Peak Oil', Non-OPEC production plateau Resources are sufficient to meet future demand. Estimates from the US Geological Survey of ultimately recoverable reserves have doubled since the early 1980s, while cumulative production during this period was less than one-third of this increase.

This has been due to such factors as technology, successful exploration and enhanced recovery from existing fields. On top of this, there is a vast resource base of nonconventional oil to explore and develop.

Non-OPEC crude oil supply at first rises in the reference case to a plateau of around 48 mb/d, before beginning a gradual decline from around 2020. This plateau is initially maintained as increases from Latin America (chiefly Brazil), Russia and the Caspian compensate for decreases elsewhere, mainly in the North Sea. The Middle East and Africa region experiences a slight rise in volumes over the medium-term to 2010, but this reaches a plateau of close to 5 mb/d. Non-OPEC crude oil supply is expected to be just over 45 mb/d in 2030.

Biofuels, non-conventional oil Regarding non-conventional oil supply and biofuels from non-OPEC countries, the most significant growth is expected to come from the Canadian oil sands, which is seen rising in the reference case to 5 mb/d in 2030, from just 1 mb/d in 2005. Coal-to- liquids and gas-to-liquids are also expected to grow, from about 150,000 b/d and less than 50,000 b/d, to 1.5 mb/d and 500,000 b/d respectively from 2005–2030. These increases will come predominantly from the US, China, South Africa and Australia.

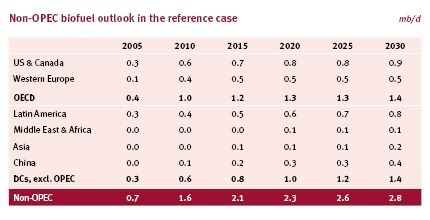

The use of biofuels is also increasing in many regions throughout the world, and recent pronouncements of ambitious targets amplify uncertainties for future demand and supply volumes. In total, the reference case sees more than 10 mb/d of nonconventional oil supply including biofuels coming from non-OPEC by 2030, 8 mb/d more than in 2005.

Of those 10 mb/d, the bulk may come from biofuels, under a high scenario:

OPEC’s projections for biofuels supply in a high scenario case, which assumes an accelerated policy push in consuming countries, sees biofuels supply at just over 5 mb/d in 2030, thus realising even lower demand for oil products in general, and for OPEC oil in particular.

Uncertainty over the magnitude of the rise in non-OPEC non-conventional supply is growing. For example, the European Union recently adopted a minimum binding target for biofuels to reach a 10% share in transport gasoline and diesel consumption.

And in the US, the most recent proposal, as reflected in the ‘Twenty In Ten Goal’, proposes alternative transport fuels hitting over 2 mb/d by 2017.

The Outlook's reference scenario for biofuel supply is extremely conservative (click to enlarge) compared to projections by other organisations (such as the IEA) or to the cumulative supply that would emerge if actual targets set by countries are met. But even in this reference case, OPEC sees the rise of biofuels as an important factor in the uncertainty over OPEC oil demand.

Demand for OPEC crude falls, stabilize, falls Initial increases in both crude and non-crude supply pushes total non-OPEC supply up to 54 mb/d in 2010. This is 5 mb/d higher than in 2005. With demand rising by only a slightly higher rate, this leaves little room for additional OPEC oil. Indeed, with OPEC non-crude supply, primarily natural gas liquids (NGLs), set to rise to just under 6 mb/d by 2010, the demand for OPEC crude by 2010 is almost 1 mb/d below 2005 levels.

After 2010, non-OPEC crude supply, including NGLs, stabilises, then eventually falls. Yet with non-conventional oil supply increasing at strong rates, over the entire projection period, total non-OPEC supply actually continues to rise. The amount of crude oil supply expected from OPEC increases post-2010, rising, in this reference case, to 38 mb/d by 2020 and 49 mb/d by 2030.

Investments in capacity These projections underline the need for substantial investment along the entire supply chain. Expansion of non-OPEC capacity is two-to-three times more costly than in OPEC, with this gap widening over time. The highest cost region is the OECD, which also experiences the highest decline rates. Up to 2030, total upstream investment requirements, from 2006 onwards, amount to $2.4 trillion (in 2006 US$).

These estimates, however, do not include necessary infrastructure investments. Concerning crude oil price assumptions for medium- to long-term analyses, it has been observed that the oil industry, guided by the recent price trends, has mostly revised upward the business-as-usual price assumptions. A further observation is that, due to the effect of several factors, economic growth and oil demand are both now more resilient to higher oil prices than had previously been thought.

All these trends, in addition to rising costs, have become integral to the general perception of higher expected prices in the long-term. Continuous downward revisions to demand projections from organizations such as the International Energy Agency and the US Department of Energy/Energy Information Administration are also noted. In this regard, a key question is whether this downward revision process is set to continue.

On the supply side, there has been a steady rise in expectations for non-OPEC production in the longer term. Increased attention is being paid to non-conventional oil and biofuels and a discernibly higher expected contribution to supply is emerging.

Uncertainty over demand There is a great deal of uncertainty over future demand and non-OPEC supply, which translates into large uncertainties over the amount of oil that OPEC Member Countries will eventually need to supply. Investment requirements are very large, and subject to considerably long lead-times and pay-back periods. It is therefore essential to explore these uncertainties in the context of alternative scenarios.

Downside risks to demand are more substantial than upside potential. There is a range of important drivers, in particular energy and environmental policies in consuming countries and technological developments, tending to reduce demand.

Uncertainties over future oil demand translate into a wide range of possible levels of necessary investment in OPEC Member Countries. Even over the medium-term to 2010, there is an estimated range of uncertainty of $50 billion for required investment in the upstream, increasing to $140 billion by 2015. This is part of why security of demand is a key concern for producers.

The expected increase in demand for oil products translates into a rising volume of crude that needs refining. Therefore, it is essential to focus attention upon the downstream sector as this is also a key element of the supply chain, and ultimately of market stability. In addition to rising demand, there is a continued move towards lighter and cleaner products. To meet this type of demand, the downstream sector will require significant investment to ensure that sufficient distillation capacity is in place, supported by adequate conversion, desulphurisation, as well as all other secondary processes and facilities.

The reference case for refining capacity expansion estimates that over 7 mb/d of new capacity — out of 14 mb/d of announced projects — will be added to the refining system globally by 2012. Almost 70% of the new capacity will be in the Middle East and Asia-Pacific. With capacity creep, the global reference case capacity additions from existing projects could reach just over 9 mb/d by 2015.

Other drivers of capacity creep However, several factors will add to the downside risk in the reference case. Mainly because of rising downstream sector construction costs in recent years, combined with the difficulties in finding skilled labour and experienced professionals, these figures have the potential to change. This risk is further exacerbated by the reluctance of refiners to expedite the implementation of projects in light of the rapidly changing policies that put a strong emphasis on developing alternative fuels that compete directly with refined products.

These issues play out in the alternative cost-driven delayed scenario for short- and medium-term capacity expansion. In this scenario, the new distillation capacity additions could be reduced to as low as 8 mb/d for the period until 2015, including assumed capacity creep.

Recognising this, it is evident that up to 2010, refinery capacity expansion under the reference case for refinery projects just keeps pace with the required incremental refinery throughputs. The deficit is small, but does not indicate any potential easing of refinery capacity and utilisations in the shorter term. The cost-driven delayed scenario for capacity additions worsens the deficit.

Nevertheless, under the reference case outlook for refinery projects, the data indicates that capacity additions should exceed requirements in 2011 and 2012 as a range of new projects comes on stream, thereby easing refining tightness and potentially margins.

Under the cost-driven delayed scenario, the excess additions relative to reference requirements are essentially eliminated. Moreover, if global oil demand growth moves below reference case levels, then an easing in the refining sector could begin as early as 2008.

Uncertain projections for biofuels There are uncertainties surrounding these projections. This is especially relevant for biofuels. In general, biofuels projects do not take as long to implement as refinery projects. The reference case allows for a significant medium-term increase in biofuels production. Any additional increase would further reduce required refinery throughputs and margins. Consequently, policy initiatives to support the development of biofuels may discourage refiners, as well as possibly crude oil producers, from investing in the needed capacity expansion.

Should such a situation be followed by biofuels failing to meet the stated targets, the result could be further tightness in the downstream, and possibly the upstream, and in turn, this could have a significant impact on prices, margins and volatility.

Biofuels also raises issues over the future structure of a complex downstream sector that includes both oil and biofuels. The question is how the sector should be structured in order to withstand major disruptions. With the increasing number of biofuel producers, the chances of losing this capacity for a longer period and over a larger area, for example due to drought, could easily lead to a shortage of required fuels.

Let us remark that OPEC forgets that biofuels are being and will produced in many different countries and regions - projects can be planned and energy crops grown virtually anywhere, unlike oil which has to be 'discovered' - , so a local drought will only marginally affect global supply. A terrorist attack on one big oil refinery, a pipeline, or a major well would have much more impact.

In any case, the Outlook states that under these circumstances, the follow-up question is whether refiners should hold sufficient spare capacity to cover potential losses. OPEC Member Countries have offered, and will continue to offer, an adequate level of upstream spare capacity for the benefit of the world at large.

Downstream investment in consuming nations It is equally important, however, that adequate capacity also exists in the downstream sector at all times, which is primarily the responsibility of consuming nations.

Based on the reference case assessment of known projects, by 2015 a total of almost 2 mb/d of additional distillation capacity will be required, and by 2020, a further 3.7 mb/d. This is what is needed, on top of the assessed likely capacity additions, to bring the global refining system back into long-run balance, with refining margins that allow for a return on investment, but are not as tight as those of today.

Taking into account the most likely changes in the future supply and demand structures and their quality specifications, the global downstream sector will require in the period 2006–2020, 13 mb/d of additional distillation capacity, around 7.5 mb/d of combined upgrading capacity, 18 mb/d of desulphurisation capacity and 2 mb/d of capacity for other supporting processes, such as alkylation, isomerisation and reforming.

The total required investment in refinery processing to 2020 is projected to be $450 billion in the reference case. Of this, $110 billion comprises the cost of known projects, $110 billion covers the further required process unit additions and $230 billion comprises the ongoing maintenance and replacement. The Asia-Pacific requires the highest level of investment in new units to 2020, with China accounting for around 75% of the Asia-Pacific total.

Inter-regional oil trade should increase by 13 mb/d to almost 63 mb/d of oil exports in 2020. Both crude and products exports will increase appreciably, with products exports growing faster than crude oil exports. Correspondingly, the reference case outlook calls for a total tanker fleet requirement in 2020 of 460 million dwt. This compares to 360 million dwt as of the end of 2006.

Environmentally driven regulations also play an important role in respect to the refined products quality specifications. Clearly, this trend is set to continue in the future, creating a potential for market fragmentation unless regulations are introduced in a co-ordinated manner. Therefore, future quality regulations should, as much as possible, ensure the fungibility of fuels to avoid shortages and prevent unnecessary volatility in product and crude oil markets.

The U.S. Department of Energy (DOE) Secretary Samuel W. Bodman announced yesterday that the DOE will invest up to $375 (€279) million in three new Bioenergy Research Centers that will be located in Oak Ridge, Tennessee; Madison, Wisconsin; and near Berkeley, California.

The Centers are intended to accelerate basic research in the development of cellulosic ethanol and other biofuels, advancing President Bush’s Twenty in Ten Initiative, which seeks to reduce U.S. gasoline consumption by 20 percent within ten years through increased efficiency and diversification of clean energy sources. The Department plans to fund the Centers for the first five years of operation (Fiscal Years 2008-2013).

These Centers will provide the transformational science needed for bioenergy breakthroughs to advance President Bush’s goal of making cellulosic ethanol cost-competitive with gasoline by 2012, and assist in reducing America’s gasoline consumption by 20 percent in ten years. The collaborations of academic, corporate, and national laboratory researchers represented by these centers are truly impressive and I am very encouraged by the potential they hold for advancing America’s energy security. - U.S. Energy Secretary Samuel W. Bodman

To bring the latest tools of the biotechnology revolution to bear to advance clean energy production, the Centers will be supported by multidisciplinary teams of top scientists. A major focus will be on understanding how to reengineer biological processes to develop new, more efficient methods for converting the cellulose in plant material into ethanol or other biofuels that serve as a substitute for gasoline. This research is critical because future biofuels production will require the use of feedstocks more diverse than corn, including cellulosic material like agricultural residues, grasses, poplar trees, inedible plants, and non-edible portions of crops.

The Centers will bring together diverse teams of researchers from 18 of the nation’s leading universities, seven DOE national laboratories, at least one nonprofit organization, and a range of private companies. All three Centers are located in geographically distinct areas and will use different plants both for laboratory research and for improving feedstock crops: bioenergy :: biofuels :: energy :: sustainability :: ethanol ::biomass :: cellulose :: biotechnology :: biorefinery :: United States :: The mission of the Bioenergy Research Centers will lie at the frontier between basic and applied science, and will maintain a focus on bioenergy applications. These Centers aim to identify real steps toward practical solutions regarding to the challenge of producing renewable, carbon-neutral energy. At the same time, the Centers will be grounded in basic research, pursuing alternative avenues and a range of high-risk, high-return approaches to finding solutions. To some degree, one key to the Centers’ success will be their ability to develop the more basic dimensions of their research to a point that can easily transition to applied research.

The Department’s three Bioenergy Research Centers will include:

The DOE BioEnergy Science Center led by the DOE’s Oak Ridge National Laboratory in Oak Ridge, Tennessee. The Center Director will be Martin Keller, and collaborators include: Georgia Institute of Technology in Atlanta, Georgia; DOE’s National Renewable Energy Laboratory in Golden, Colorado; University of Georgia in Athens, Georgia; Dartmouth College in Hanover, New Hampshire; and the University of Tennessee, in Knoxville, Tennessee.

The DOE Great Lakes Bioenergy Research Center will be led by the University of Wisconsin in Madison, Wisconsin, in close collaboration with Michigan State University in East Lansing, Michigan. The Center Director will be Timothy Donohue, and other collaborators include: DOE’s Pacific Northwest National Laboratory in Richland, Washington; Lucigen Corporation in Middleton, Wisconsin; University of Florida in Gainesville, Florida; DOE’s Oak Ridge National Laboratory in Oak Ridge, Tennessee; Illinois State University in Normal, Illinois; and Iowa State University in Ames, Iowa.

The DOE Joint BioEnergy Institute will be led by DOE’s Lawrence Berkeley National Laboratory. The Institute Director will be Jay Keasling, and collaborators include: Sandia National Laboratories; DOE’s Lawrence Livermore National Laboratory; University of California - Berkeley; University of California - Davis; and Stanford University in Stanford, California.

Subject to the finalization of contract terms and congressional appropriations, the Centers are expected to begin work in 2008, consistent with President Bush’s Fiscal Year 2008 Budget Request, and would be fully operational by 2009. DOE’s Office of Science issued a competitive Funding Opportunity Announcement in August 2006 to solicit applications. The three Centers were chosen following a merit-based, competitive review process that included external scientific peer review of the applications.

The establishment of the bioenergy research centers culminates a six-year effort by DOE’s Office of Science to lay the foundation for breakthroughs in systems biology for the cost-effective production of renewable energy. In July 2006, DOE’s Office of Science issued a joint biofuels research agenda with the Department’s Office of Energy Efficiency and Renewable Energy titled "Breaking the Biological Barriers to Cellulosic Ethanol".The report provides a detailed roadmap for cellulosic ethanol research, identifying key roadblocks and areas where scientific breakthroughs are needed.

Today’s announcement follows other key funding announcements this year to advance President Bush’s Twenty in Ten Initiative, and to make cellulosic ethanol cost competitive with gasoline by 2012. On February 28, 2007, DOE announced up to $385 million for six biorefinery projects that when fully operational are expected to produce more than 130 million gallons of cellulosic ethanol per year. On May 1, 2007, DOE announced a funding opportunity for $200 million over five years (FY’07-FY’11) to support the development of small scale bio-refineries that produce liquid transportation fuels such as ethanol. Read additional information on DOE’s biofuels initiatives.

Additional information is available on the Department’s three Bioenergy Research Centers and the Department’s Genomics Research Programs.

DOE's Office of Science is the single largest supporter of basic research in the physical sciences in the nation and helps ensure U.S. world leadership across a broad range of scientific disciplines. The Office of Science supports a diverse portfolio of research at more than 300 colleges and universities nationwide, manages ten world-class national laboratories with unmatched capabilities for solving complex interdisciplinary scientific problems, and builds and operates the world’s finest suite of scientific facilities and instruments used annually by more than 19,000 researchers to extend the frontiers of all areas of science.

References: U.S. Department of Energy (DOE) Biomass Program.

International research effort underway to sequence cassava genome, which may result in increased starch yields - USDA Agricultural Research Service - Aug. 30, 2006

Cassava has one of the highest rates of CO2 fixation and sucrose synthesis for any C3 plant. With this in mind, researchers from Ohio State University develop transgenic cassava with starch yields up 2.6 times higher than normal plants by increasing the sink strength for carbohydrate in the crop. This means cassava makes for a 'super crop' when it comes to both CO2 fixation and carbohydrate production, i.e. sugars, the feedstock for ethanol - Plant Biotechnology Journal - Volume 4/Issue 4 - July 2006

Vietnam's Institute of Tropical Biology to invest in Jatropha research - Le courrier du Vietnam - Sept. 6, 2006

Genetic study proves humans have pushed orangutans to the brink of extinction; genetic decline coincides with establishment of oil palm plantations in Malaysia/Indonesia since the 1950/60s- Public Library of Science / BiologyVolume 4/Issue 2 - February, 2006

Researchers at the International Institute for the Semi-Arid Tropics have developed a sweet sorghum for the production of ethanol. The new variety has a very high sugar content in its root. Average yields in trial fields in the Philippines were between 95 to 125 tons, considerably higher than those of sugarcane - ICRISAT - Feb. 28, 2007

Sokoine University of Agriculture, Tanzania, develops sorghum and millet processing technologies suitable for local conditions in effort to empower small farmers - IPP Media - Sept. 6, 2006

South Africa blocks GM Sorghum project for fears over contamination of local wild sorghums - Kruger Park - Aug. 26, 2006

Brazilian authorities have given their fiat for field trials with genetically modified sugar cane plants. The Centro de Tecnologia Canavieira (Cane Technology Center - CTC) will test three genetically modified varieties that are expected to yield 15% more sugar - GMO Compass

The International Eucalyptus Genome Consortium's sequencing effort has been taken up as a project under the U.S. Dept. of Energy's Joint Genome Project for the year 2008. - Biopact June 12, 2007

Brazilian state of Acre intends to make cattle ranchers reforest land which they have cleared for grazing. The sustainable forestry policy is based on replanting economic tree crops such as mahogany, acai, Brazil nut and palms - BBCNews Sept. 27, 2006

Illegal deforestation of acacia for charcoal is becoming a serious problem in Kenya's Naivasha area. Nobel Peace Prize laureate Wangari Maathai's Green Belt Movement re-afforests with acacia but needs more support to win fight against illegal loggers - Kenya Times Sept. 5, 2006

Australian scientists are conducting a 'time-machine' experiment to see how eucalyptus trees cope with increased levels of CO2 and global warming. - University of Western Sydney Aug. 28, 2006

Bamboo planting can slow deforestation, scientists from the International Center for Research in Agroforestry in Nairobi, Kenya, say. Bamboo rapidly becoming economically beneficial crop with large potential for energy, bioremediation, and afforestation - Chosun (S.Korea) Aug. 30, 2006

"The beauty of miscanthus is that you only have to sow it once...Because of the way it grows, there is no need for fertilisers or chemicals", an English entrepreneur talks about his experience with Miscanthus as an energy crop - Grantham Today Aug. 8, 2006

Petro-Canada and GreenField Ethanol have inked a long-term deal that makes Petro-Canada the exclusive purchaser of all ethanol produced at GreenField Ethanol's new facility in Varennes, Quebec. The ethanol will be blended with gasoline destined for Petro-Canada retail sites in the Greater Montreal Area.

Petro-Canada and GreenField Ethanol have inked a long-term deal that makes Petro-Canada the exclusive purchaser of all ethanol produced at GreenField Ethanol's new facility in Varennes, Quebec. The ethanol will be blended with gasoline destined for Petro-Canada retail sites in the Greater Montreal Area.

The two Danish biotechnology firms Novozymes A/S and Xergi A/S, heavily involved in the biofuels sector, have announced an agreement that enables them to collaborate on the co-development of microorganisms and environmental technologies for the optimal harvest of energy from manure products for use in the production of renewable biogas that yields electricity, heat, and fuels, as well as high-quality fertilizer. According to the Danish Board of Technology, biomethane from manure can supply 25% of the energy required by the Danish transport sector.

The two Danish biotechnology firms Novozymes A/S and Xergi A/S, heavily involved in the biofuels sector, have announced an agreement that enables them to collaborate on the co-development of microorganisms and environmental technologies for the optimal harvest of energy from manure products for use in the production of renewable biogas that yields electricity, heat, and fuels, as well as high-quality fertilizer. According to the Danish Board of Technology, biomethane from manure can supply 25% of the energy required by the Danish transport sector. bioenergy :: biofuels :: energy :: sustainability :: biogas :: biomethane :: fertilizer :: enzymes :: anaerobic fermentation :: Denmark ::

bioenergy :: biofuels :: energy :: sustainability :: biogas :: biomethane :: fertilizer :: enzymes :: anaerobic fermentation :: Denmark :: According to BBC Brasil, a Chinese state-owned enterprise and a Brazilian group have

According to BBC Brasil, a Chinese state-owned enterprise and a Brazilian group have

The U.S. Department of Energy (DOE) Secretary Samuel W. Bodman

The U.S. Department of Energy (DOE) Secretary Samuel W. Bodman

Wednesday, June 27, 2007

WWF condemns Planktos Inc. iron-seeding plan in the Galapagos

Scientists have warned against this type of 'geo-engineering' schemes, which have - in the case of iron seeding - clearly shown not to work and could harm ocean life (previous post). Simulations also indicate that such strategies carry considerable environmental risks and could even worsen the effects of climate change (earlier post). For these reasons, the UN's Intergovernmental Panel for Climate Change has clearly stated in its latest report that none of these techniques carry a priority to mitigate climate change (report of the IPCC's Working Group III).

One of those far more feasible and less risky geo-engineering options is the implementation of carbon-negative bioenergy systems (also known as 'Bio-Energy with Carbon Storage' or BECS, see earlier post, and here, here).

According to a summary by the United States Government submitted to the International Maritime Organization, Planktos, Inc. - a for-profit company - will dump up to 100 tons of iron dust this month in a 36 square mile area located approximately 350 miles west of the Galapagos Islands. Planktos, Inc. plans to dump the iron in international waters using vessels neither flagged under the United States nor leaving from the United States so U.S. regulations such as the U.S. Ocean Dumping Act do not apply and details do not need to be disclosed to U.S. entities:

Potential negative impacts of the Planktos experiment include:

- Shifts in the composition of species that make up plankton, the base of the marine food chain, would cause changes in all the species that depend on it.

- The impact of gases released by both the large amount of phytoplankton blooms induced by Planktos, Inc. and resulting bacteria after the phytoplankton die.

- Bacterial decay following the induced phytoplankton bloom will consume oxygen, lowering oxygen levels in the water and changing its chemistry. This change in chemistry could favor the growth of microbes that produce powerful greenhouse gases such as nitrous oxide.

- The introduction of large amounts of iron to the ecosystem - unless it is in a very pure form, which is likely cost-prohibitive at the scales proposed - would probably be accompanied by other trace metals that would be toxic to some forms of marine life.

In the waters around the Galapagos, some 400 species of fish swim with turtles, penguins and marine iguanas above a vast array of urchins, sea cucumbers, crabs, anemones, sponges and corals. Many of these animals are found nowhere else on earth.If you feel like protesting against Planktos Inc.'s questionable experiment - we do - then join us in writing to the company to express your concerns. Send your email to Russ George, CEO of Planktos Inc.:[email protected].

Reference:

Eurekalert: World Wildlife Fund warns against plan by Planktos, Inc. - June 27, 2007.

Article continues

posted by Biopact team at 5:35 PM 0 comments links to this post