The Intergovernmental Panel on Climate Change (IPCC) kicks off the meeting in Valencia, Spain, which will result in the production of the Synthesis Report on climate change. The report will summarize the core findings of the three volumes published earlier by the separate working groups.

The Intergovernmental Panel on Climate Change (IPCC) kicks off the meeting in Valencia, Spain, which will result in the production of the Synthesis Report on climate change. The report will summarize the core findings of the three volumes published earlier by the separate working groups.

Global Bioenergy Partnership issues report on current state, challenges and benefits of bioenergy

The Global Bioenergy Partnership (GBEP) has presented its report, A review of the current state of bioenergy development in G8 +5 countries [*.pdf], today during the 20th World Energy Congress (WEC) in Rome. The analysis provides a survey of the production of energy and fuels from biomass in G8 +5 countries (Brazil, China, India, Mexico and South Africa), highlighting the benefits and challenges of "one of the future’s most promising alternative energy sources". The report looks at the current level of production, at policies, the market situation, trade and standards. Finally, it analyses the urgent need for the development of mechanisms to ensure sustainable production.

The Global Bioenergy Partnership (GBEP) has presented its report, A review of the current state of bioenergy development in G8 +5 countries [*.pdf], today during the 20th World Energy Congress (WEC) in Rome. The analysis provides a survey of the production of energy and fuels from biomass in G8 +5 countries (Brazil, China, India, Mexico and South Africa), highlighting the benefits and challenges of "one of the future’s most promising alternative energy sources". The report looks at the current level of production, at policies, the market situation, trade and standards. Finally, it analyses the urgent need for the development of mechanisms to ensure sustainable production.Interestingly, the GBEP notes that the case for a 'Biopact' remains strong:

International trade in biofuels and related feedstocks may provide win-win opportunities for some countries: for several developed countries imports are a necessary precondition for meeting the self-imposed blending targets; for several developing countries producing and exporting biofuels may provide new business opportunities and new end-markets for their agricultural products. For small and medium-sized developing countries, export markets may be necessary to initiate their industries, however, tariffs and other barriers are currently restricting trade.Bioenergy has rapidly emerged as a top priority on the international agenda. The GBEP builds its activities upon three strategic pillars: energy security, food security and sustainable development. It was established to implement the commitments taken by the G8 +5 Countries in the 2005 G8 Summit in Gleneagles, and was recently invited by the G8 Summit in Heiligendamm to “continue its work on biofuel best practices and take forward the successful and sustainable development of bioenergy”.

This can offset lower production costs in producing countries, represent significant barriers to international trade, and have negative repercussions on investments in the sector. A more liberal trade regime would greatly contribute to the achievement of the economic, energy, environmental and social goals that countries are pursuing.

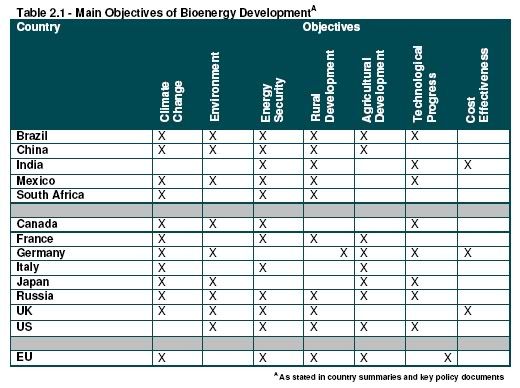

The GBEP's first comprehensive report finds that the reasons to promote the rapid growth of the sector are shared by most countries (table, click to enlarge):

The GBEP's first comprehensive report finds that the reasons to promote the rapid growth of the sector are shared by most countries (table, click to enlarge):- rising oil prices and energy security considerations are forcing countries to look for alternative fuels;

- biofuels can play a role in rural development, providing energy access to remote communities and creating employment;

- last but certainly not least, climate change benefits that can be realized through reduction of GHG emissions

Production

According to the best data available, bioenergy provides about 10 percent of the world’s total primary energy supply (47.2 EJ of bioenergy out of a total of 479 EJ in 2005, i.e. 9.85 percent). Most of this is for use in the residential sector (for heating and cooking) and is produced locally. In 2005 bioenergy represented 78 percent of all renewable energy produced. A full 97 percent of biofuels are made of solid biomass, 71 percent of which used in the residential sector. Biomass is also used to generate gaseous and liquid fuels, and growth in demand for the latter has been significant over the last ten years (graph, click to enlarge):

According to the best data available, bioenergy provides about 10 percent of the world’s total primary energy supply (47.2 EJ of bioenergy out of a total of 479 EJ in 2005, i.e. 9.85 percent). Most of this is for use in the residential sector (for heating and cooking) and is produced locally. In 2005 bioenergy represented 78 percent of all renewable energy produced. A full 97 percent of biofuels are made of solid biomass, 71 percent of which used in the residential sector. Biomass is also used to generate gaseous and liquid fuels, and growth in demand for the latter has been significant over the last ten years (graph, click to enlarge): energy :: ethanol :: biodiesel :: biomass :: bioenergy :: biofuels :: climate change :: sustainability :: energy security :: rural development :: Global Bioenergy Partnership ::

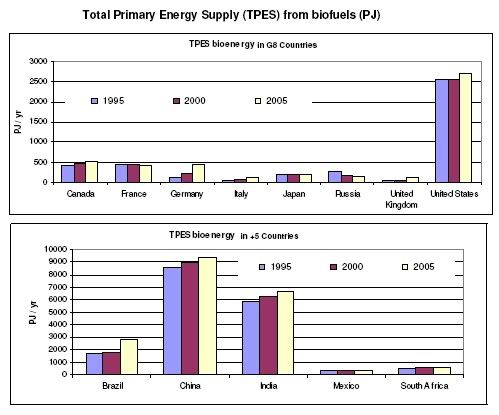

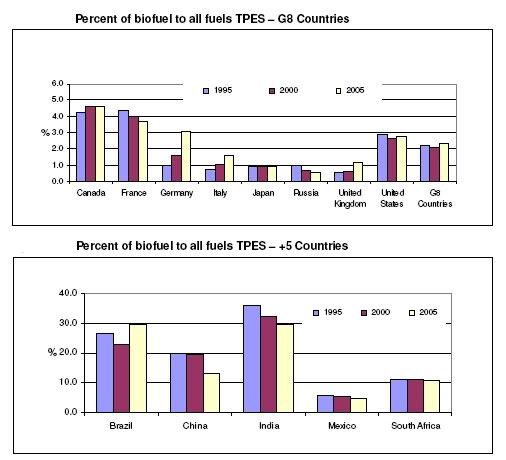

energy :: ethanol :: biodiesel :: biomass :: bioenergy :: biofuels :: climate change :: sustainability :: energy security :: rural development :: Global Bioenergy Partnership ::  Biomass provides a relatively small amount of the total primary energy supply (TPES) of the G8 Countries (1-4 percent). By contrast, bioenergy is a significant part of the energy supply in the +5 Countries representing from 5-27 percent of TPES. China with its 9000 PJ/yr is the largest user of biomass as a source of energy, followed by India (6000 PJ/yr), USA 2300 PJ/yr, and Brazil (2000 PJ/yr), while bioenergy’s contribution in Canada, France and Germany is around 450 PJ/yr (graph, click to enlarge).

Biomass provides a relatively small amount of the total primary energy supply (TPES) of the G8 Countries (1-4 percent). By contrast, bioenergy is a significant part of the energy supply in the +5 Countries representing from 5-27 percent of TPES. China with its 9000 PJ/yr is the largest user of biomass as a source of energy, followed by India (6000 PJ/yr), USA 2300 PJ/yr, and Brazil (2000 PJ/yr), while bioenergy’s contribution in Canada, France and Germany is around 450 PJ/yr (graph, click to enlarge).The share of 'primitive' bioenergy use in India, China and Mexico is decreasing, mostly as traditional biomass is substituted by kerosene and LPG. However the use of solid biomass for electricity production is important, especially from pulp and paper plants. Bioenergy’s share in total energy consumption is increasing in the G8 Countries especially Germany, Italy and the United Kingdom.

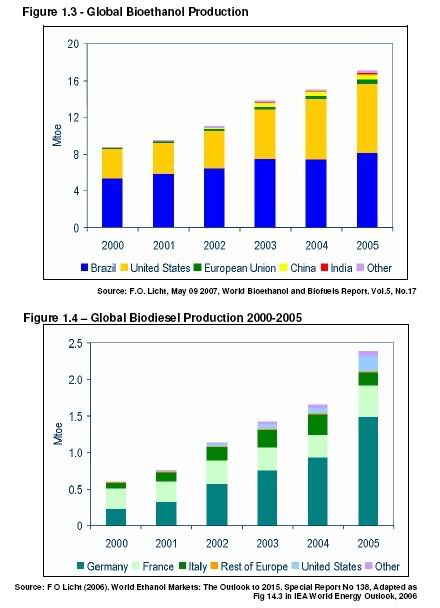

The production of liquid biofuels - both biodiesel and ethanol - for transport is increasing rapidly in all countries. Brazil is leading the production of ethanol, mainly from sugarcane, whereas Germany is at the forefront of biodiesel production (graph, click to enlarge).

The production of liquid biofuels - both biodiesel and ethanol - for transport is increasing rapidly in all countries. Brazil is leading the production of ethanol, mainly from sugarcane, whereas Germany is at the forefront of biodiesel production (graph, click to enlarge).There are four key factors driving interest in bioenergy: rising prices for fossil fuels, in particular oil prices; energy security; climate change; and rural development. Bioenergy markets are largely policy dependent in most of the world, as the production of biofuels in most countries is not at this point competitive with fossil fuels. Nearly all countries reported that energy security and climate change are the most important drivers of their bioenergy development activities.

Policy measures

Overall there are few differences between the policy objectives of G8 Countries and the +5 Countries. Rural development is more central to the +5 Countries’ focus on bioenergy development, and this is often aligned with a poverty alleviation agenda.

Overall there are few differences between the policy objectives of G8 Countries and the +5 Countries. Rural development is more central to the +5 Countries’ focus on bioenergy development, and this is often aligned with a poverty alleviation agenda.Feed-in tariffs, taxes, guaranteed markets (i.e. renewable energy and fuel mandates, and preferential purchasing), compulsory grid connections, other direct supports (i.e. grants, loan guarantees, subsidies, construction incentives, etc.), and R,D&D are the principal policy mechanisms being deployed by the G8 +5 Countries to encourage bioenergy development (table, click to enlarge).

Bioenergy markets are further influenced by general energy, agriculture and forestry, climate change, and environmental policies.

Feed-in tariffs are currently the world’s most widespread national renewable energy policy and are in use in over half of the G8 +5 Countries. They are often crafted for renewable energy generally but are sometimes directed at bioenergy specifically. The feed-in tariff is the policy tool that has been most effective in stimulating renewable energy markets, however feed-in tariffs need to be differentiated by technology and biomass treated individually, in order to specifically boost bioenergy.

A variety of tax incentives and penalties are used by governments to foster bioenergy development and they are one of the most widely used support instruments. Taxes affect the cost-competitiveness of bioenergy vs. substitutes and therefore bioenergy viability in the marketplace.

National targets and public incentive systems have been effectively used in many countries, in particular for liquid biofuels for transport. Among the G8 +5 Countries, only Russia has not created a transport biofuel target. Voluntary quota systems or targets are common for biomass energy for heat, power and transport fuels in the G8 Countries, however, blending mandates enforceable via legal mechanisms are becoming increasingly utilized.

Blending targets are less established in the +5 Countries but they are under discussion or awaiting approval. Preferential purchasing by governments can also be a powerful tool when effectively implemented. In policies relating to biofuels for transport, there is a trend towards policies such as blending mandates which don’t require direct government funding, although publicly financed support remains significant.

Most countries use some form of direct loans or grants. The G8 +5 Governments are conducting research and development in their own laboratories and institutes and many are supporting public private partnerships and various forms of demonstration projects. Direct supports and R,D&D are being used in a number of G8 Countries to accelerate the commercial development of second generation biofuels for transportation.

A few governments are moving towards performance focused policies. Rather than mandate an amount of fuel to be consumed, these governments are mandating the amount of GHG reductions required. This strategy to harness market forces is rapidly gaining interest in Kyoto signatory countries that are looking for the most cost-effective GHG emission strategies.

Sustainability

There is a growing recognition that not all biofuels are “green.” New schemes are under way to promote sustainability as well as link funding to sustainability. The European Union and some of its member states are working toward sustainability standards to attach to mandatory targets. Brazil has created its “social seal” and has tied it to its blending mandates.

No international sustainability assurance system exists for biofuels or bioenergy more broadly. Several international processes to create such a system are underway, however, even these do not deal with all concerns due to the potential for impact shifting. This occurs when feedstock from existing fields/plantations is used for biofuels that was originally used for other applications which leads to unsustainably produced feedstocks being used, or to new plantations/fields being created, to supply these other applications. The fungibility of feedstocks, land, and other inputs for feed, fuel, and food is leading some to call for a universal framework for sustainability requirements.Ultimately, the GBEP says, sustainability requirements will need to be agreed upon internationally, applied locally, and applied to all biomass regardless of end use if leakage effects or impact shifting is to be avoided.

Enforcement is critical to the functioning of any of these schemes. While a discussion of enforcement strategies is beyond the scope of this summary, it must be acknowledged as central. The capacity of countries to enforce protections, or even to enact them in the first place, is highly variable. In many developing countries, where much of the investment interest is focused, the pressure to reduce regulations and oversight in order to attract foreign investment is an additional challenge. These factors point to the need for international assurance systems.

Trade and standards

There is a move towards harmonization of technical standards regionally and internationally. This is vital for quality assurance, equipment compatibility, and the facilitation of trade. Historically, biomass and biofuel trade flows have been limited, as most of the production has been for domestic consumption. However, in the coming years, international trade in biofuels and feedstocks is expected to escalate rapidly to satisfy increasing worldwide demand.

The World Trade Organization (WTO) does not currently have a trade regime specific to biofuels. International trade in biofuels falls, therefore, under the rules of the General Agreement on Tariffs and Trade (GATT 1994). In addition to the WTO, several regional and bilateral trade agreements, mostly involving the United States and the EU, currently regulate biofuels trade.

International trade in biofuels and related feedstocks may provide win-win opportunities for some countries: for several developed countries imports are a necessary precondition for meeting the self-imposed blending targets; for several developing countries producing and exporting biofuels may provide new business opportunities and new end-markets for their agricultural products. For small and medium-sized developing countries, export markets may be necessary to initiate their industries, however, tariffs and other barriers are currently restricting trade.

The GBEP concludes that government policies play a key role in influencing investment in bioenergy. When carefully balanced with environmental and social conditions, such policies will also determine the long-term viability of this important emerging opportunity.

In February 2007, the Global Bioenergy Partnership recommended the preparation of this Report on the current state of bioenergy development in G8 + 5 Countries as a reference platform for future work of GBEP towards the sustainable development of bioenergy. Development of the Report was guided by the Food and Agriculture Organization of the United Nations (FAO), under the coordination of Gustavo Best and Jeff Tschirley with the support of Astrid Agostini and Maria Michela Morese (GBEP Secretariat). The lead author of this Report is Suzanne Hunt with supporting inputs from Rudi Drigo and staff contributions on the country summaries from the Italian Ministry for the Environment Land and Sea, and UN Foundation.

References:

Global Bioenergy Partnership: A review of the current state of bioenergy development in G8 +5 countries [*.pdf] - November, 2007.

0 Comments:

Post a Comment

Links to this post:

Create a Link

<< Home