Brasil Ecodiesel, the leading Brazilian biodiesel producer company, recorded an increase of 57.7% in sales in the third quarter of the current year, in comparison with the previous three months. Sales volume stood at 53,000 cubic metres from August until September, against 34,000 cubic metres of the biofuel between April and June. The company is also concluding negotiations to export between 1,000 to 2,000 tonnes of glycerine per month to the Asian market.

Brasil Ecodiesel, the leading Brazilian biodiesel producer company, recorded an increase of 57.7% in sales in the third quarter of the current year, in comparison with the previous three months. Sales volume stood at 53,000 cubic metres from August until September, against 34,000 cubic metres of the biofuel between April and June. The company is also concluding negotiations to export between 1,000 to 2,000 tonnes of glycerine per month to the Asian market.

World Energy Council: advanced biofuels can replace over 40% of petrofuels by 2050, most promising solution to reduce GHG emissions

Passenger vehicle transportation and aviation are expected to remain dependent on oil for the foreseeable future, but alternative fuels and propulsion systems will increase their penetration considerably, a study published by the World Energy Council (WEC) says. The WEC report on 'Transport Technologies and Policy Scenarios to 2050' outlines the results of an analysis conducted by a group of international WEC transport experts and gives concrete policy recommendations to develop sustainable transport systems. The experts identified next-generation biofuels as the most promising option to ensure a transition towards sustainable mobility.

The study looks at the prospects for alternative liquid fuels, hydrogen, (plug-in) hybrids, electric vehicles and other technologies. For non-liquid fuels and propulsion technologies (hydrogen, battery-electric cars) biomass is seen as a leading renewable primary energy source to be used for the production of renewable hydrogen and green electricity.

Large potential for next-generation biofuels

In 2050, gasoline and diesel are likely to remain the dominant fuels, the study states, but the portion of advanced biofuels such as biomass-to-liquids (BTL, also known as 'synthetic biofuels') and cellulosic ethanol are set to grow considerably.

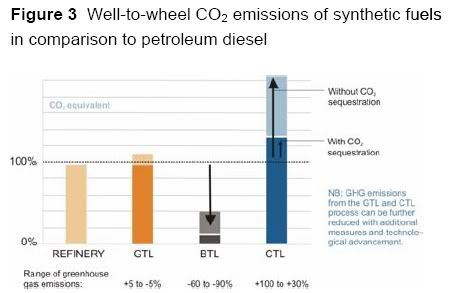

The WEC also sees BTL fuels and cellulosic ethanol achieving the greatest reductions in GHG emissions as they reduce CO2 emissions by up to 90% (graph, click to enlarge). Other synthetic fuels such as gas-to-liquids (GTL) and coal-to-liquids (CTL) increase accessibility and availability by diversifying the fuel supply base and, in particular with GTL, are already available and economically viable. These fuels have the same physical properties as BTL and therefore exhibit the same advantages in distribution and use.

The WEC also sees BTL fuels and cellulosic ethanol achieving the greatest reductions in GHG emissions as they reduce CO2 emissions by up to 90% (graph, click to enlarge). Other synthetic fuels such as gas-to-liquids (GTL) and coal-to-liquids (CTL) increase accessibility and availability by diversifying the fuel supply base and, in particular with GTL, are already available and economically viable. These fuels have the same physical properties as BTL and therefore exhibit the same advantages in distribution and use.

On a life cycle basis, GHG emissions from GTL are comparable to those from conventional diesel fuel. GHG emissions from CTL without carbon capture and storage are approximately double those from conventional diesel fuel. The development and production of CTL and GTL also contribute to technological experience and understanding of synthetic fuels in general, which will benefit the development of BTL in the long term.

In particular, the WEC sees significant benefits in BTL fuels. Their contribution to reduced petroleum consumption is immediate, they can be used in new and existing vehicles, they are not limited by new infrastructure requirements and they can contribute in all transport sectors which consume liquid fuels (land passenger and freight as well as shipping and aviation). Other advanced biofuels are under development and may present viable long-term options with lower primary energy consumption.

Due to their currently increasing penetration and the investments made in their production, conventional first generation biofuels such as ethanol from sugar cane or corn and biodiesel (or hydro-treated vegetable oil, which has similar properties to BTL) from oil-bearing plants can be expected to retain some market share in the long term.

Since there is a large number of biofuels in production or under investigation, it is important to ensure the most efficient solutions prevail. For a longterm sustainable penetration, biofuels must be drawn into production according to market forces and viable, consistently applied GHG intensity and sustainability standards, without discrimination, rather than chosen according to government mandates. The WEC sees global free trade in biofuels as 'essential':

The WEC expects internal combustion engines (ICEs) to remain dominant, but advanced concepts for internal combustion will emerge, including processes such as homogeneous charge compression ignition (HCCI), with the objective of combining the advantages of diesel and gasoline:

energy :: sustainability :: climate change :: fossil fuels :: oil :: biofuels :: cellulosic ethanol :: biomass-to-liquids :: electric vehicles :: hydrogen :: biomass ::

energy :: sustainability :: climate change :: fossil fuels :: oil :: biofuels :: cellulosic ethanol :: biomass-to-liquids :: electric vehicles :: hydrogen :: biomass ::

Hydrogen fuel and fuel cell vehicles are expected to gain a market foothold by 2035 and grow towards 2050. On-board electric power utilisation in personal transport will also increase, in particular in OECD and richer developing countries, which have more economic capacity to absorb the cost premium over conventional vehicle concepts.

This will initially be manifested as increased hybridisation. A significant presence of pure electric vehicles powered by batteries and/or fuel cells is a potential scenario, assuming that progress on the necessary technologies and their costs is sufficient to enable a commercially viable product.

Improvements in efficiency and reductions in consumption will likely remain based on the diesel engine, which is currently dominant in this sector.

Innovations in engine performance will be shared with the passenger vehicle diesel sector and include variable valve timing and new combustion techniques such as HCCI. Hybridisation, which has already penetrated in certain applications, can be expected to increase in popularity. In particular, urban buses have found a niche hybrid segment, which will likely expand. Certain short-haul and even long-haul trucks may also be considered for some type of hybridisation, due to the significant amounts of braking energy that can be recuperated. Alternative and biofuels also apply to this sector.

Aviation fuels

In aviation, engine and materials technologies and flight management measures will potentially be available which can improve aircraft efficiency by over 30%. Set against the expected 200% growth in air travel by 2050, efficiency improvements can serve to dampen the projected increase in consumption.

Aviation fuel presents a particular opportunity for alternative fuels, since aviation fuel (kerosene) can be, and is already, made using the synthetic Fischer-Tropsch process, which can use gas, coal or biomass as a feedstock (GTL, CTL and BTL fuels).

Hydrogen and fuel cells

One particular technology that holds significant longterm potential for reduction in fossil energy consumption, as well as CO2 and criteria exhaust emissions, is hydrogen, which offers the long-term promise of emissions-free driving. Hydrogen and fuel cells have the potential to contribute significantly in the passenger vehicle sector if the substantial challenges of fuel cell cost, hydrogen storage, hydrogen production and hydrogen delivery can be overcome.

Current fuel cell vehicle concepts demonstrate that the potential exists for fuel cell vehicles to provide convenient personal transport in the kind of vehicles to which consumers are accustomed. Therefore, the motivation to overcome the obstacles mentioned above is significant and solutions are being developed by manufacturers, engineers and governments.

The commercial vehicle sector appears to have less potential in applying hydrogen and fuel cell technology, due in part to the large space necessary for fuel storage, especially on long-haul trucks. However, the eventual maturity of hydrogen technology in the passenger vehicle sector is a foundation on which this sector may also be able to build in the long term, and indeed the use of fuel cells as auxiliary power units in trucks has already been tested.

A long-term hydrogen strategy must be based on sustainable hydrogen production and consider the well-to-wheel energy and emissions in relation to conventional forms of propulsion. Local production of hydrogen using renewable energy is already being developed and applied in many regions. However, for hydrogen fuel to comprise a substantial proportion of the transportation market, the energy required to produce it must be derived from the general power grid.

Therefore, a hydrogen economy must go hand in hand with widespread sustainable power generation to provide a successful future scenario. Assuming adequate supply, significant technical advances and investments are necessary in the distribution and delivery of hydrogen fuel.

Battery technologies

Battery electric vehicles (BEVs) have potentially greater energy savings potential than hydrogen fuel cells, due to the higher energy efficiency of batteries. However, battery technology and cost must improve substantially to provide the performance, range and affordability demanded by consumers. In particular, significant increases in energy storage density are required in order to store sufficient energy on board for adequate vehicle range, if BEVs are to penetrate the mainstream.

Electric powertrains are initially likely to make advances in small vehicles for city driving (city electric vehicle – CEV), in which range and top performance are of lesser importance and since economic incentives for low emission vehicles in cities are becoming more popular. A number of commercial companies are already offering vehicles to this CEV niche whilst others are offering electric vehicles as a sporty premium product.

Plug-in hybrid electric vehicles (PHEVs) offer most of the benefits of BEVs with the convenience and range of conventional internal combustion engines. These combine a reduced ICE and a high power battery, such that pure electric driving is possible over a range high enough for many daily applications, allowing overnight charging from an electric socket.

The presence of two full powertrains in a PHEV means that for this technology to become viable for the mass market, substantial reductions in the cost of the electric powertrain are essential. For both BEVs and PHEVs, enhanced battery durability for these deep discharge applications (as opposed to shallow discharge in current hybrids) is necessary, in order for the battery to last as long as an expected vehicle lifetime of many years.

Recommendations for sustainable mobility

According to the WEC, policymakers must first agree on the overall objective, whether it be a reduction in energy consumption or greenhouse gas emissions. From there, technological development must be complemented by rational policy that will encourage and enable the technologies to emerge. The common thread in policymaking is that the market must be allowed to identify and advance the most efficient methods to reach the stated objective. Conversely, selecting specific technologies through direct mandates or beneficial treatment runs the strong risk of selecting inappropriate technologies and therefore not contributing adequately to the objective.

Applying the integrated approach

The integrated approach incorporates all the measures described above and therefore commits all stakeholders to contribute to achieving the energy solution. Each element of the approach can be a stand-alone item. However, the approach achieves the most by ensuring that the task of reducing energy consumption is equitably distributed between the sectors and stakeholders involved.

Since the costs of energy reduction are different in each sector, and indeed vary between measures applied within each sector, the most effective overall result is achieved by concentrating on the least-cost measures.

Theoretically, the ideal way to determine the least cost methods and to bring them into being is to ensure a consistent economic incentive for energy reduction across all sectors. Due to the complexity of each sector and the different ways in which price signals are communicated (through vehicles, fuels, ticket prices etc), such a consistent incentive is difficult to identify. It has been suggested by economists and policymakers that carbon taxes or emissions trading schemes can be an effective solution and indeed emissions trading has been introduced in the European Union to cover GHG emissions from certain sectors.

In the absence of such a consistent market signal, any policy decisions which incentivise or regulate actions in the transport sector should be subject to independent and objective assessments. It must be recognised that in the long term, micromanagement of energy policy will create overcomplexity andinefficiency and all policy options must support a longterm strategy to ensure a functioning market, which is then incentivised and enabled to achieve the energy objectives. This ensures that the burden is shared equitably between sectors, that the costs for society are minimised and that the most effective and efficient measures are identified and receive encouragement.

The methods described by the WEC support the integrated approach and ensure that the energy objective is targeted in a way that brings the maximum benefit to users of transport and to society as a whole. This promotes in the most effective way the achievement of sustainable energy for all.

References:

World Energy Council: Transport Technologies and Policy Scenarios to 2050 [*.pdf], October 2007.

The study looks at the prospects for alternative liquid fuels, hydrogen, (plug-in) hybrids, electric vehicles and other technologies. For non-liquid fuels and propulsion technologies (hydrogen, battery-electric cars) biomass is seen as a leading renewable primary energy source to be used for the production of renewable hydrogen and green electricity.

Large potential for next-generation biofuels

In 2050, gasoline and diesel are likely to remain the dominant fuels, the study states, but the portion of advanced biofuels such as biomass-to-liquids (BTL, also known as 'synthetic biofuels') and cellulosic ethanol are set to grow considerably.

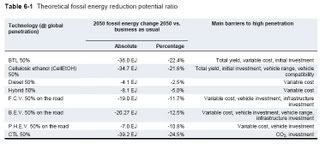

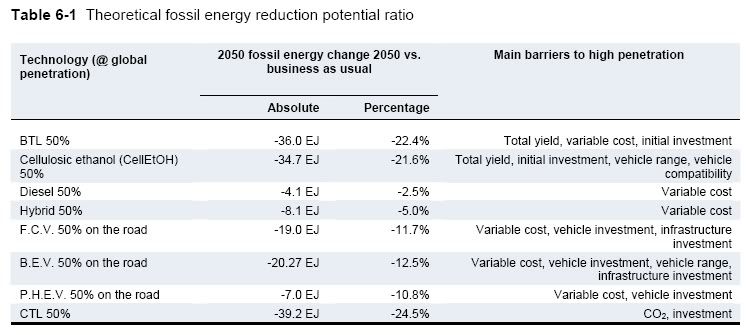

Theoretical fossil energy reduction potential ratio of different fuels and propulsion technologies.

The study sees the highest potential for reduction in petroleum and fossil energy, and therefore greenhouse gases, in biofuels. Under a set of breakthrough scenarios biofuels can replace 300% of all petrofuels, but a more likely scenario is a 50% global penetration of BTL in diesel fuel with a 50% overall diesel passenger vehicle penetration in 2050 and a total BTL plant efficiency of 60%. This would result in a reduction of 22.4% of all petroleum used in transport by 2050. Cellulosic ethanol can replace 21.6% of global fossil transport fuels. Hybrids, plug-in hybrids, electric vehicles and fuel cell vehicles have a far smaller reduction potential (table, click to enlarge). The WEC also sees BTL fuels and cellulosic ethanol achieving the greatest reductions in GHG emissions as they reduce CO2 emissions by up to 90% (graph, click to enlarge). Other synthetic fuels such as gas-to-liquids (GTL) and coal-to-liquids (CTL) increase accessibility and availability by diversifying the fuel supply base and, in particular with GTL, are already available and economically viable. These fuels have the same physical properties as BTL and therefore exhibit the same advantages in distribution and use.

The WEC also sees BTL fuels and cellulosic ethanol achieving the greatest reductions in GHG emissions as they reduce CO2 emissions by up to 90% (graph, click to enlarge). Other synthetic fuels such as gas-to-liquids (GTL) and coal-to-liquids (CTL) increase accessibility and availability by diversifying the fuel supply base and, in particular with GTL, are already available and economically viable. These fuels have the same physical properties as BTL and therefore exhibit the same advantages in distribution and use.On a life cycle basis, GHG emissions from GTL are comparable to those from conventional diesel fuel. GHG emissions from CTL without carbon capture and storage are approximately double those from conventional diesel fuel. The development and production of CTL and GTL also contribute to technological experience and understanding of synthetic fuels in general, which will benefit the development of BTL in the long term.

In particular, the WEC sees significant benefits in BTL fuels. Their contribution to reduced petroleum consumption is immediate, they can be used in new and existing vehicles, they are not limited by new infrastructure requirements and they can contribute in all transport sectors which consume liquid fuels (land passenger and freight as well as shipping and aviation). Other advanced biofuels are under development and may present viable long-term options with lower primary energy consumption.

Due to their currently increasing penetration and the investments made in their production, conventional first generation biofuels such as ethanol from sugar cane or corn and biodiesel (or hydro-treated vegetable oil, which has similar properties to BTL) from oil-bearing plants can be expected to retain some market share in the long term.

Since there is a large number of biofuels in production or under investigation, it is important to ensure the most efficient solutions prevail. For a longterm sustainable penetration, biofuels must be drawn into production according to market forces and viable, consistently applied GHG intensity and sustainability standards, without discrimination, rather than chosen according to government mandates. The WEC sees global free trade in biofuels as 'essential':

Further support for the market through free global trade in biofuels is essential, both to ensure the most energetically effective biofuels have access to the market and to assist in the economic and energy development of lower income countries.Propulsion technologies

The WEC expects internal combustion engines (ICEs) to remain dominant, but advanced concepts for internal combustion will emerge, including processes such as homogeneous charge compression ignition (HCCI), with the objective of combining the advantages of diesel and gasoline:

energy :: sustainability :: climate change :: fossil fuels :: oil :: biofuels :: cellulosic ethanol :: biomass-to-liquids :: electric vehicles :: hydrogen :: biomass :: Hydrogen fuel and fuel cell vehicles are expected to gain a market foothold by 2035 and grow towards 2050. On-board electric power utilisation in personal transport will also increase, in particular in OECD and richer developing countries, which have more economic capacity to absorb the cost premium over conventional vehicle concepts.

This will initially be manifested as increased hybridisation. A significant presence of pure electric vehicles powered by batteries and/or fuel cells is a potential scenario, assuming that progress on the necessary technologies and their costs is sufficient to enable a commercially viable product.

Improvements in efficiency and reductions in consumption will likely remain based on the diesel engine, which is currently dominant in this sector.

Innovations in engine performance will be shared with the passenger vehicle diesel sector and include variable valve timing and new combustion techniques such as HCCI. Hybridisation, which has already penetrated in certain applications, can be expected to increase in popularity. In particular, urban buses have found a niche hybrid segment, which will likely expand. Certain short-haul and even long-haul trucks may also be considered for some type of hybridisation, due to the significant amounts of braking energy that can be recuperated. Alternative and biofuels also apply to this sector.

Aviation fuels

In aviation, engine and materials technologies and flight management measures will potentially be available which can improve aircraft efficiency by over 30%. Set against the expected 200% growth in air travel by 2050, efficiency improvements can serve to dampen the projected increase in consumption.

Aviation fuel presents a particular opportunity for alternative fuels, since aviation fuel (kerosene) can be, and is already, made using the synthetic Fischer-Tropsch process, which can use gas, coal or biomass as a feedstock (GTL, CTL and BTL fuels).

Hydrogen and fuel cells

One particular technology that holds significant longterm potential for reduction in fossil energy consumption, as well as CO2 and criteria exhaust emissions, is hydrogen, which offers the long-term promise of emissions-free driving. Hydrogen and fuel cells have the potential to contribute significantly in the passenger vehicle sector if the substantial challenges of fuel cell cost, hydrogen storage, hydrogen production and hydrogen delivery can be overcome.

Current fuel cell vehicle concepts demonstrate that the potential exists for fuel cell vehicles to provide convenient personal transport in the kind of vehicles to which consumers are accustomed. Therefore, the motivation to overcome the obstacles mentioned above is significant and solutions are being developed by manufacturers, engineers and governments.

The commercial vehicle sector appears to have less potential in applying hydrogen and fuel cell technology, due in part to the large space necessary for fuel storage, especially on long-haul trucks. However, the eventual maturity of hydrogen technology in the passenger vehicle sector is a foundation on which this sector may also be able to build in the long term, and indeed the use of fuel cells as auxiliary power units in trucks has already been tested.

A long-term hydrogen strategy must be based on sustainable hydrogen production and consider the well-to-wheel energy and emissions in relation to conventional forms of propulsion. Local production of hydrogen using renewable energy is already being developed and applied in many regions. However, for hydrogen fuel to comprise a substantial proportion of the transportation market, the energy required to produce it must be derived from the general power grid.

Therefore, a hydrogen economy must go hand in hand with widespread sustainable power generation to provide a successful future scenario. Assuming adequate supply, significant technical advances and investments are necessary in the distribution and delivery of hydrogen fuel.

Battery technologies

Battery electric vehicles (BEVs) have potentially greater energy savings potential than hydrogen fuel cells, due to the higher energy efficiency of batteries. However, battery technology and cost must improve substantially to provide the performance, range and affordability demanded by consumers. In particular, significant increases in energy storage density are required in order to store sufficient energy on board for adequate vehicle range, if BEVs are to penetrate the mainstream.

Electric powertrains are initially likely to make advances in small vehicles for city driving (city electric vehicle – CEV), in which range and top performance are of lesser importance and since economic incentives for low emission vehicles in cities are becoming more popular. A number of commercial companies are already offering vehicles to this CEV niche whilst others are offering electric vehicles as a sporty premium product.

Plug-in hybrid electric vehicles (PHEVs) offer most of the benefits of BEVs with the convenience and range of conventional internal combustion engines. These combine a reduced ICE and a high power battery, such that pure electric driving is possible over a range high enough for many daily applications, allowing overnight charging from an electric socket.

The presence of two full powertrains in a PHEV means that for this technology to become viable for the mass market, substantial reductions in the cost of the electric powertrain are essential. For both BEVs and PHEVs, enhanced battery durability for these deep discharge applications (as opposed to shallow discharge in current hybrids) is necessary, in order for the battery to last as long as an expected vehicle lifetime of many years.

Recommendations for sustainable mobility

According to the WEC, policymakers must first agree on the overall objective, whether it be a reduction in energy consumption or greenhouse gas emissions. From there, technological development must be complemented by rational policy that will encourage and enable the technologies to emerge. The common thread in policymaking is that the market must be allowed to identify and advance the most efficient methods to reach the stated objective. Conversely, selecting specific technologies through direct mandates or beneficial treatment runs the strong risk of selecting inappropriate technologies and therefore not contributing adequately to the objective.

1. An integrated approach: in order to meet the defined objective, an integrated approach is the most efficient overall concept, which applies a holistic methodology rather than concentrating only on one element of a solution, for example technologies. The integrated approach incorporates all relevant stakeholders in the chain of energy production and use, to apply effective energy saving measures and technologies. These stakeholders include actors in equipment manufacturing, commercial businesses, consumers and policymakers.

The approach addresses the behaviour of business and private consumers in their vehicle purchasing decisions, vehicle use and behaviour. Fuel suppliers have a role due to the energy content of their fuels. The technology and investment applied by the equipment manufacturers determines the efficiency of their vehicles. Governments and other policymaking bodies have a responsibility for the transportation infrastructure and environment as well as the incentive structure for certain types of public behaviour. It must be ensured that for all stakeholders a productive market is in place which financially rewards behaviour leading to higher efficiency.

2. Incentives for takeholders:

2.1. Vehicle manufacturers: vehicle, engine and component technologies do indeed comprise a major element of this approach. Therefore, effective policy can take the form of incentives through the tax system for fuel and vehicle technologies which reduce energy consumption or GHG emissions. Such incentives must be applied in a way that provides a consistent incentive to reduce consumption or GHG emissions (depending on the priority objective). For example, a tax that varies in a proportional fashion with vehicle consumption rating creates such an incentive. The marginal tax level should be sufficient to provide an incentive to purchase a vehicle despite the higher initial cost of its efficiency technologies, but not so high as to distort the market or make purchases unaffordable. Such taxes need not mean a higher overall tax burden, since taxes based on consumption or emissions can be offset by reductions in other taxes, for example by replacing vehicle registration taxes.

In addition, government financial support for bringing new technologies to market is appropriate if objectively assessed and effectively targeted. Such support can be provided as an investment at any point in the technology value chain, from basic research, product development, production facilities, entrepreneurship and product marketing. It should be directed to those products and the point in the value chain which is objectively assessed to provide the greatest incremental leverage in meeting the long- term energy objective compared to incremental investment.

2.2. Infrastructures: Governments should also invest in infrastructure for both private and public transport to minimise congestion, ensure convenience and mobility, support economic growth and contribute to the energy objectives.

2.3. Consumers: consumers should be educated as to the consequences of their transportation decisions, in particular by sufficient labelling of, and information on, personal vehicles, fuels and public transport options. In addition, consumer education is required on the efficiency of use of energy consuming products. In transportation this specifically refers to driving style in personal and commercial vehicles, in which less aggressive driving, more efficient gear changes, predictive behaviour (when approaching traffic lights or congestion) and switching off when idle can reduce per-vehicle consumption significantly.

2.4. Fuel suppliers: The fossil energy and carbon content of fuels is a further element in total energy consumption. As is currently under discussion in the EU, the US Federal Government and at the US state level (California), carbon intensity standards for transportation fuels are being developed. These policies set targets for reducing the fossil and carbon content of fuels and the fuel suppliers will select the most efficient methods for reducing CO2 emissions. This can be expected to promote the use of biofuels with low well-to-wheel CO2 emissions, as well as reduce the energy intensity of producing conventional and alternative fuels. Incentives through the tax system or otherwise can also apply to fuels, as long as these are applied consistently, without discrimination and proportional to the energy or environmental objective that is being sought.

3. StandardsThe latter point is very important because with it the WEC joins those who call for the abolishment of the current tariffs in place in the EU and the US, which prevent much more efficient and sustainable biofuels produced in the South to enter the market. With advanced biofuels, biomass productivity and cost of the primary feedstocks remains a key factor; countries in the tropics and the semi-tropics have many agro-ecological advantages here, which they should be allowed to exploit to the fullest. This way, biofuels can not only become a strong weapon in the fight against climate change, but a tool for development in poor countries.

Common standards within and between major markets are essential to support technical and market development. In particular, standards relating to conventional and alternative fuels are a key element in energy and climate policy, including the carbon intensity standards described above. Standards relating to conventional, alternative and biofuels are already in place and include quality norms which ensure that the fuels are compatible with the existing vehicle stock and with new vehicles.

Applied to biofuels, these regulate their physical and chemical characteristics and the proportion that can be blended with petroleum based fuels. They should remain sufficiently rigorous to ensure increased penetration of biofuels is consistent with vehicle reliability. Ideally, such standards should be aligned between major global markets. In addition, standards for biofuels should include sustainability criteria relating to land use and social factors, which are developed and applied consistently and without discrimination to all biofuels.

These standards thereby support the market in its economic selection of the most efficient solutions whilst contributing to the achievement of the energy objective. Indeed, such standards are being considered in parallel to fuel quality and carbon intensity.

Further support for the market through free global trade in biofuels is essential, both to ensure the most energetically effective biofuels have access to the market and to assist in the economic and energy development of lower income countries.

Applying the integrated approach

The integrated approach incorporates all the measures described above and therefore commits all stakeholders to contribute to achieving the energy solution. Each element of the approach can be a stand-alone item. However, the approach achieves the most by ensuring that the task of reducing energy consumption is equitably distributed between the sectors and stakeholders involved.

Since the costs of energy reduction are different in each sector, and indeed vary between measures applied within each sector, the most effective overall result is achieved by concentrating on the least-cost measures.

Theoretically, the ideal way to determine the least cost methods and to bring them into being is to ensure a consistent economic incentive for energy reduction across all sectors. Due to the complexity of each sector and the different ways in which price signals are communicated (through vehicles, fuels, ticket prices etc), such a consistent incentive is difficult to identify. It has been suggested by economists and policymakers that carbon taxes or emissions trading schemes can be an effective solution and indeed emissions trading has been introduced in the European Union to cover GHG emissions from certain sectors.

In the absence of such a consistent market signal, any policy decisions which incentivise or regulate actions in the transport sector should be subject to independent and objective assessments. It must be recognised that in the long term, micromanagement of energy policy will create overcomplexity andinefficiency and all policy options must support a longterm strategy to ensure a functioning market, which is then incentivised and enabled to achieve the energy objectives. This ensures that the burden is shared equitably between sectors, that the costs for society are minimised and that the most effective and efficient measures are identified and receive encouragement.

The methods described by the WEC support the integrated approach and ensure that the energy objective is targeted in a way that brings the maximum benefit to users of transport and to society as a whole. This promotes in the most effective way the achievement of sustainable energy for all.

References:

World Energy Council: Transport Technologies and Policy Scenarios to 2050 [*.pdf], October 2007.

5 Comments:

Biopact might wish to do an article based on

http://www.chron.com/disp/story.mpl/chronicle/5195599.html

We will pick up 25%, Immediately, when the first auto company builds the first E85-"optimized" engine.

The approx. 30% differential in Octane between gasoline (86) and Ethanol (113) means that ethanol in the proper engine (Higher Compression, such as the Indy Car engines) will actually attain a slightly Higher "efficiency" (up to 42%) than either Diesel, or gasoline.

Why this Octane differential goes unremarked, upon, even in reports supportive of biofuels is beyond me. It, absolutely, changes all calculations, remarkably.

For example: When an American medium haul trucker such as Yellow Roadway realizes they can save over 30% on his fuel costs by going to a high-compression engine running E85 the world will "change."

This will take longer in the EU, of course, since the much higher taxes on transport fuels tend to mask, or at least diminish, the effect of price differentials in the base fuel product.

Hi David, as you may have read, Biopact will only cover developments in algae-to-fuels when they are breakthroughs.

Recently Green Fuels carried out a test (after its infamous 'successful failure' of last time), and claims to have achieved high yields. Obviously, the test was carried out in the most optimal summer month. We want to see results for an entire year.

There's plenty of research showing how algae yields drop considerably in winter, autumn and spring. But that algae company never mentions this.

In order to calm down the algae hype, we will only report on developments that signify a real breakthrough. So far, none have been reported. But this will surely change.

Cheers,

Jonas

Could someone tell me what really is "the inconvenient truth" between those 2? Check this out:

http://www.greencarcongress.com/2007/09/study-for-oecd-.html#more

OECD and WEC studies offer 2 paradoxical visions of the Energy issues and solutions in 2050. Which one to trust? Or maybe "The truth is out there"...

Rem

There really isn't any contradiction between both studies. The WEC report looks at the potential of many different biofuels over the long term. It was written by 20 or so energy experts.

The working paper presented to the OECD Roundtable zooms in on subsidies and tariffs for first generation biofuels. It was written by two activists who expose the problems arising from subsidies. One of them Ron Steenblik, heads the Global Subsidies Initiative.

So the two reports look at different things.

But when it comes to estimating the sustainable potential of biofuels, I would go for studies by the experts of the WEC or the International Energy Agency, not so much for the subsidy specialists.

Post a Comment

Links to this post:

Create a Link

<< Home